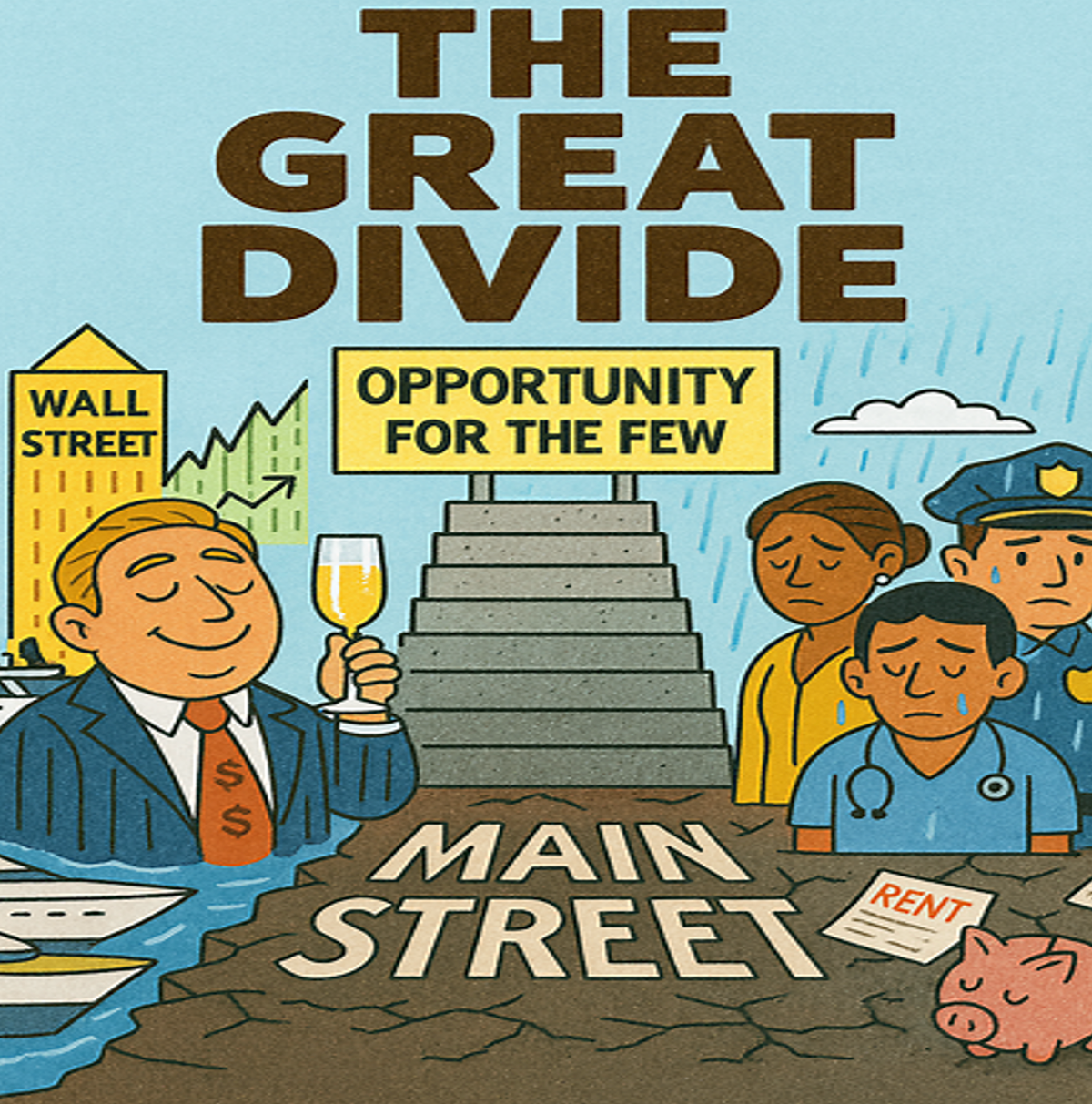

America -- The Land of the Great Divide

Thoughts on the Market

November 11, 2025

This week I want to address what I see as a terrifying trend in the United States, one that could one day rip this great country apart. I am labeling this trend “The Great Divide.” Over the past forty years the U.S. economy has increasingly split into a two-tiered system: one tier for the wealthy, and another for everyone else. This divide is now so stark that economists describe ours as a “K-shaped economy,” where the rich continue to rise while, in an almost mirror image, the rest fall behind.

The term “K-shaped economy” generally refers to how different groups have fared since the 2008 financial crisis – and especially after the COVID-19 pandemic – but this trend has roots that run much deeper than just the past seventeen years. Although it certainly has accelerated during this period, upper-income Americans have seen strong income growth, booming stock portfolios, and rising home values for many decades. Meanwhile, low- and middle-income Americans – people like teachers, tradespeople, law enforcement, skilled medical technicians, hospitality workers – have faced stagnant wages, rising debt, and progressively unaffordable housing and healthcare. The typical American family now has two wage earners but is still struggling financially.

Wealth Concentration at the Top

- As of 2025, the top 10% of earners own nearly two-thirds of all U.S. wealth, while the bottom 50% hold just 2.5%.

- Since 1989, the top 1% gained 987 times more wealth per household than the bottom 20%.

- The top 0.1% alone gained an average of $39.5 million per household, while the bottom 20% gained less than $8,500 in the same period.

Everyday Americans Are Struggling

- Housing: Home prices have outpaced wage growth, pushing first-time buyers to a record age of 40.

- Debt: Student loans, credit cards, and medical bills weigh heavily on younger and working-class Americans.

- Job insecurity: Gig work and contract jobs offer flexibility but little stability or benefits.

Billionaire Boom vs. Working-Class Bust

- The U.S. now has more billionaires than any other country, with individuals like Elon Musk holding over $340 billion in personal wealth.

- Meanwhile, 7.4% of households earn under $15,000 a year, not nearly enough to cover basic needs.

- Consumer confidence is near record lows while the stock market and housing prices are at, or near, all-time highs. This is a disconnect that spells very serious trouble for the future.

This divide, however, isn’t just economic -- it’s social and political. This type of economy can lead to devastating long-term consequences including weakened economic growth, political instability, reduced social mobility, and systemic financial risk.

Here’s a more detailed breakdown of the implications:

1. Slower Economic Growth

- Reduced Consumer Demand: When most income gains go to the wealthy, overall consumption suffers. This is because when their income grows, the rich often save more, while the rest of the population cuts spending, slowing GDP growth.

- Underinvestment in Human Capital: Lower and middle income households struggle to afford education, healthcare, and housing, limiting workforce productivity and innovation.

- Regional Disparities: Wealth concentration in urban centers leaves rural and post-industrial regions behind, creating economic deserts.

2. Political Polarization and Instability

- Erosion of Trust: Perceived unfairness in economic outcomes undermines faith in institutions and democratic norms.

- Rise of Populism: Economic frustration fuels support for populist movements and leaders who promise radical change, often at the expense of long-term stability.

- Policy Gridlock: Diverging interests between economic classes can lead to legislative paralysis, especially around taxation, healthcare, and education.

- Consolidation of Political Power: The fact is that wealthy people have the power to drive many of the government’s laws and policies, thus further reinforcing this dangerous trend.

3. Financial System Vulnerabilities

- Debt Dependency: Lower-income households increasingly rely on credit to maintain living standards, raising delinquency rates and systemic risk (as seen in rising credit card defaults).

- Asset Inflation: Wealthy investors drive up prices of stocks, real estate, and other assets, creating bubbles that can destabilize markets.

- Banking Risk: A bifurcated economy pressures banks to serve high-risk borrowers while catering to elite wealth management, increasing exposure to volatility.

4. Decline in Social Mobility

- Education Gaps: Quality education becomes a privilege, not a right, reinforcing generational inequality.

- Housing Segregation: Rising home prices and rents push working families out of opportunity-rich areas.

- Labor Market Stratification: High-paying jobs cluster in tech and finance, while service and gig work dominate for the rest, with limited upward mobility.

5. Cultural and Psychological Effects

- Mental Health Strain: Economic insecurity contributes to stress, anxiety, and depression, especially among younger and marginalized populations.

- Social Fragmentation: Class divides erode shared identity and civic engagement, weakening community bonds.

- Generational Cynicism: Younger Americans may lose faith in the “American Dream,” opting out of traditional paths like homeownership or family formation.

What Could Reverse the Trend?

- Progressive Tax Reform: Closing loopholes and taxing wealth could fund public investment.

- Universal Access to Higher Education and Healthcare: Reducing barriers to opportunity would help level the playing field.

- Labor Empowerment: Strengthening unions and wage protections could rebalance power in the workplace.

- Affordable Housing Initiatives: Expanding access to stable housing would support mobility and community stability.

Another way to reverse the trend would be highly unpleasant but I believe is becoming increasingly likely – a catastrophic correction in the stock and housing markets. I will touch on this more a little later in this write-up.

Looking at the astonishing shift in the average age of a first-time homebuyer in the U.S. gives good sense of how these trends play out in tangible ways. Consider this: the average age of a first-time homebuyer in the U.S. has increased dramatically over the past forty-five years -- from 29 in 1981 to a record-high 40 years old in 2025.

This dramatic rise reflects deep shifts in housing affordability and economic pressures:

Age Trends Over Time

- 1981: Median age was 29 years old

- 2020: Rose to 33 years old

- 2022: Increased to 36 years old

- 2024: Climbed to 38 years old

- 2025: Now at 40 years old, the highest ever recorded

Affordability Crisis

- Home prices have surged over 25% since 2019, with the median sale price now over $410,000

- High mortgage rates: Rates have nearly doubled since 2021, making monthly payments harder to manage

- Student debt and rent burden: Younger buyers are struggling to save for down payments

- Delayed life milestones: Many are postponing marriage, children, and career stability, which traditionally align with home buying

Market Impact

- First-time buyers now make up only 21% of the market, down from a long-term average of 38%

- Equity loss: Delaying homeownership by a decade could cost buyers up to $150,000 in missed equity gains

Many once-great civilizations collapsed in part due to extreme wealth inequality, which undermined social cohesion, fueled unrest, and weakened their ability to adapt to crises. Notable examples include Ancient Rome, the French monarchy, and the Maya civilization.

Here’s how wealth disparity contributed to their downfall:

Ancient Rome

- Wealth Gap: By the late Republic, land and wealth were concentrated among elite patricians, while plebeians and soldiers faced poverty and displacement.

- Consequences:

- The rise of latifundia (large estates) displaced small farmers.

- Urban poor grew dependent on grain handouts.

- Political corruption and populist uprisings (e.g. Gracchi brothers, Julius Caesar) destabilized governance.

- Collapse: Economic inequality weakened Rome’s institutions, spurred civil wars and the eventual fall of the Western Roman Empire in 476 AD.

Ancien Régime France

- Wealth Gap: The nobility and clergy enjoyed tax exemptions and vast privileges, while peasants and the emerging bourgeoisie bore the tax burden.

- Consequences:

- Resentment exploded during food shortages and economic crises.

- The Estates-General revealed the deep divide between classes.

- Collapse: The French Revolution (1789) overthrew the monarchy, leading to radical social upheaval and the end of feudal privilege.

Maya Civilization

- Wealth Gap: Archaeological evidence shows increasing inequality in housing and access to resources among elites and commoners.

- Consequences:

- Elite competition and overexploitation of resources strained the environment.

- Commoners faced food insecurity and political instability.

- Collapse: Many Maya city-states were abandoned between 800–900 AD, likely due to a mix of environmental stress and social unrest exacerbated by inequality.

Late Imperial China

- Wealth Gap: Land ownership and wealth became concentrated among elite families, while peasants faced rising rents and taxes.

- Consequences:

- Peasant uprisings (e.g. Yellow Turban Rebellion) destabilized the Han Dynasty.

- Later dynasties like the Qing faced similar unrest, culminating in the Taiping Rebellion.

- Collapse: These internal fractures weakened dynastic rule and opened the door to foreign intervention and revolution.

Other Examples

- Mesopotamian city-states: Elite control of land and labor led to revolts and eventual decline.

- Inca Empire: Though highly centralized, inequality and forced labor systems contributed to vulnerability when the Spanish arrived.

Extreme inequality doesn’t guarantee collapse, but history shows it often erodes trust, fuels unrest and weakens resilience. While today’s global inequality rivals -- and in some cases exceeds -- the disparities seen in ancient civilizations, the mechanisms and scale are uniquely modern. While ancient societies had rigid class structures and elite control of land, today’s inequality is driven by financial systems, technology, and globalization.

How Today’s Inequality Compares to Ancient Patterns

1. Scale of Wealth Concentration

- Ancient Civilizations: In places like Egypt, Mesopotamia, and Rome, wealth was concentrated in land and tribute controlled by monarchs, priests, or aristocrats.

- Today: The top 1% globally own nearly half of all wealth, and the 26 richest individuals hold as much wealth as the bottom 50% of humanity.

- Modern twist: Wealth is now concentrated not just in land, but in stocks, intellectual property, and digital platforms.

2. Mobility and Opportunity

- Ancient Societies: Social mobility was rare. Birth determined status, and upward movement was nearly impossible.

- Today: Mobility exists but is increasingly constrained by education costs, housing access, and intergenerational wealth.

- Modern twist: Inequality is masked by meritocratic ideals, but structural barriers persist.

3. Political Power and Influence

- Ancient Elites: Kings and nobles wielded direct control over laws and armies.

- Modern Elites: Billionaires and corporations influence policy through lobbying, campaign financing, and media.

- Modern twist: Influence is subtler but pervasive, shaping tax laws, labor rights, and global trade.

4. Visibility and Awareness ownership

- Ancient Times: Inequality was accepted as divine or natural order.

- Today: Inequality is widely debated, tracked, and protested -- but often tolerated due to systemic inertia.

- Modern twist: Social media and data transparency make inequality more visible, but not necessarily more solvable.

So where is all of this heading? My long-term prognosis is not good. It doesn’t take very sharp insight to see how government officials cater more and more to the rich. In fact, the explicit bias is now far more blatant than I ever dreamed possible. Today, the disdain that many government officials show towards the poor and needy is reprehensible. If we simply look at the recent example of federal financial assistance for the nation’s most vulnerable people, we can see how the great divide is already sowing dangerous seeds of anger and frustration.

A good example is the recent SNAP aid controversy, which centers on the Trump administration’s attempt to freeze food assistance payments during the ongoing government shutdown. The legal battles it sparked went all the way to the Supreme Court, while very real concern mounted about widespread hunger among the roughly 42 million low-income Americans that depend on SNAP aid for basic food.

What Is SNAP?

The Supplemental Nutrition Assistance Program (SNAP) provides monthly food aid to roughly 1 in 8 Americans, helping low-income families afford groceries. It’s administered by the U.S. Department of Agriculture (USDA).

What Sparked the Controversy?

- Amid the 2025 government shutdown, the Trump administration paused full SNAP payments, citing funding constraints.

- 25 Democrat-led states sued the administration, arguing the freeze violates the Food and Nutrition Act, which mandates aid to all eligible households.

- A federal judge ordered the administration to restore full benefits by reallocating $4 billion from child nutrition funds. Many states immediately funded their citizen’s SNAP cards.

- The USDA demanded that states that issued full benefits to “undo” those payments, or risk dire financial penalties.

- Within hours, the Trump administration appealed to the Supreme Court, seeking an emergency stay to block the payments.

- The Supreme Court granted a temporary pause – essentially allowing time for the Trump administration to appeal the lower court’s decision that available funds must be used to feed hungry citizens, leaving hungry families wondering how they would buy food while the legal battle unfolds.

- At the time of writing, the game of legal ping-pong continues, but may be rendered moot if the government shutdown ends.

Impact on Families

- Millions of households still face uncertainty about November benefits; some states have already issued aid, others have issued partial aid, and still others have issued no aid to their most vulnerable citizens.

- SNAP directors are caught between federal directives and court rulings, unsure about how to proceed.

- The impact of the SNAP freeze on millions of voters has become one of the strongest levers to pressure Congress to end the shutdown and restore funding.

Why It Matters

This controversy highlights how political gridlock can jeopardize essential aid, especially for vulnerable populations. It also raises constitutional questions about executive authority and the legal obligations of federal and state agencies during shutdowns. The controversy is an easy-to-understand demonstration of how the government – which in the U.S. is supposed to be "for the people" – can be utterly callousness. It is also a stark reminder of how small the collective governmental voice of the nation’s poorest is today, because the amount of money required to feed the nation’s neediest people is a minute fraction – about 1.6% – of the government’s total budget.

My friends overseas simply can’t fathom how a strong nation like the U.S. can turn a blind eye to tens of millions of fellow citizens – many of whom are children – who are suffering because they can’t afford to eat. Looked at through a macro lens, the U.S. government, which spends roughly $7 trillion dollars in a year, finds it acceptable for its people to go hungry, just for some political maneuverings.

I am using SNAP as an example because it is the same sort of thinking that led to the downfall of many great civilizations. Please note that I am not forecasting this for America anytime soon, but surely, our priorities can include compassion and empathy for those among us who are less fortunate.

Is the political and economic crisis that arises from this sort of behavior avoidable? Yes, but we will need wise leadership to help navigate the turbulent waters of extreme wealth disparity. My bet is that before long the U.S. will face some severe existential tests. Specifically, I would bet that at least some of these existential tests will come in the form of a dramatic sell-off in stocks. Vast amounts of wealth are held in U.S. stocks, so it is logical to assume that at some point we will face the challenge of an explosive bursting of the bubble that has inflated the value of our nation’s stock market.

Do I want this to happen? Of course not, but it is looking more and more likely as the equity bubble continues to inflate. Valuations are more extended than ever before, so a snapback, when it comes, will be vicious. Whether I look at the fiscal time bomb that our government’s borrowing will face in the coming years, or if I examine one of many existential challenges that come from our two-tiered economy, a dramatic stock market sell-off is almost guaranteed at some point – and in the not very distant future. The unacceptably high level of sticky inflation is yet another reason to exercise a reasonable degree of caution now.

With that in mind, I don’t mind noting that I think we are destined for further choppy markets over the next several weeks. This is normal price action after large, sustained moves, which is why I have suggested that we take some long-term profits in gold, and have largely flatten our long exposure stocks. As I have explained, I still like gold higher over time, but it was due for a period of corrective consolidation. The rally had been enormous, and the market had gotten ahead of itself – too many people were getting bullish AFTER a tremendous run. Gold has been gyrating in a wild range for the past few weeks, while stocks have been consolidating in a tamer fashion.

Equities have had a massive run since the April lows, so at a minimum, I would expect some continued choppy price action for a while as the market tries to decide whether it has the legs for one more sharp rally before suffering an even sharper sell-off. Of course, it wouldn’t surprise me at all if stocks were to start a more sustained corrective decline in the next couple of weeks.

In currencies, I remain a bit negative on the dollar overall. I feel that the dollar’s recent strength has been corrective in nature, so we have a good chance to see a further decline in the dollar over the coming months; I am just waiting for the right time to really get aggressive. I also think cad/chf is still heavy. It had a nice corrective bounce, but it should head lower. The yen is a bit of a different animal, and I am still largely in a watching mode as far as the yen goes. I want to eventually put on a full long-yen exposure, but it is still premature. In the meanwhile, I want to wish you the very best of luck in navigating these dynamic markets.

Andy Krieger