GOLD: Stay Long — The Rally Is Structural, Not Tactical

August 20, 2025

GOLD: Stay Long — The Rally Is Structural, Not Tactical

I. Gold’s Rally Is a Vote Against Monetary Fiction

Since October 2022, we’ve maintained a core long position in gold, opportunistically adding and trimming exposure around key technical levels. After consolidating in a $400 range since mid-April 2025, gold is now poised to accelerate toward our next major target of $3,880.

This is not just a trade — it’s a referendum. Gold’s strength is a vote against:

- The dismal failure of fiat discipline

- The erosion of central bank credibility

- The dollar’s monopoly on trust

As the Fed flirts with reflation while inflation remains sticky, gold has emerged as the final settlement layer in a world recalibrating its monetary architecture.

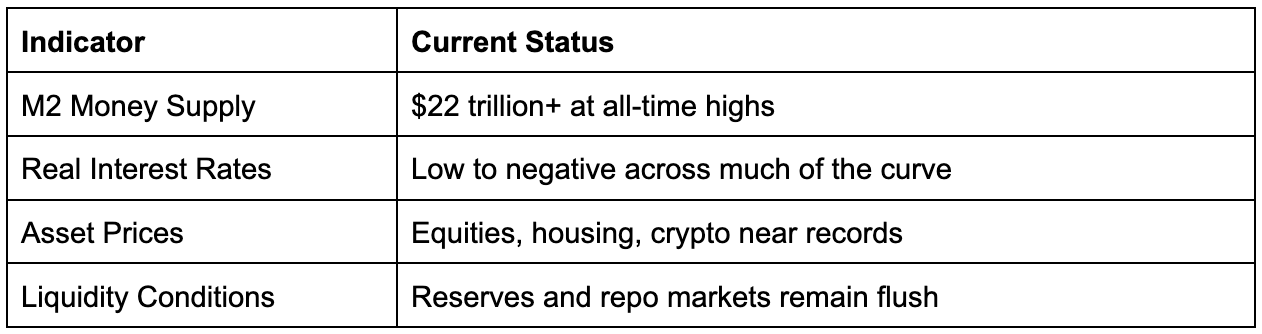

II. The Illusion of Tight Money

Despite hawkish rhetoric, monetary conditions remain loose beneath the surface:

Quantitative Tightening has been slow. The Treasury General Account rebuild has been offset by reserve injections. Net result: stimulative conditions masked by hawkish optics.

III. Gold’s Ascent: A Quiet Protest Against Monetary Theater

1. Dollar Credibility Erodes

- Central banks accumulating gold at record pace (China, India, Russia)

- Real rate suppression favors gold

- Geopolitical hedging intensifies amid U.S.–China tensions and election volatility

- DXY weakness signals erosion of monetary trust

2. Portfolio Rebalancing Begins

- Gold outperforms equities and bonds

- Institutional allocators reweight toward hard assets

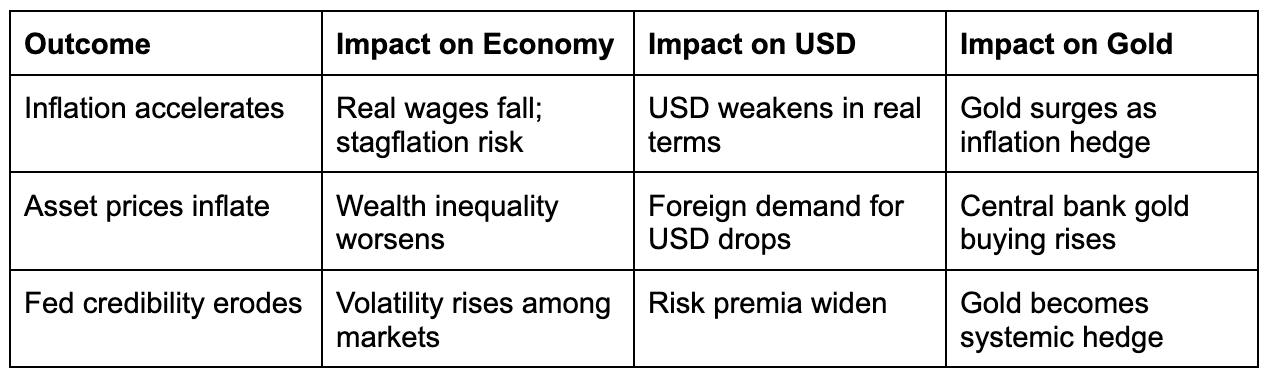

3. Inflation Expectations Unanchored

- Persistent gold strength implies expected monetary accommodation

- Fed credibility erodes; risk premia widen

4. Geopolitical Hedging Accelerates

- Trade fragmentation and reserve weaponization drive gold demand

- Dollar’s role as neutral settlement layer is challenged

IV. What If the Fed Cuts While Inflation Is Sticky?

This would echo the 1970s: cutting too early, losing inflation control, and triggering a credibility crisis.

V. Strategic Positioning

Gold’s rally is not a tactical trade —it’s a structural signal. It reflects a slow-motion exit from dollar-centric trust and a recalibration of global reserves toward neutral collateral.

“Gold isn’t just rallying — it’s indicting. Stay long, stay loud, and stay hedged.”

VI. Portfolio Implications

- Increase allocation to gold and gold-linked assets as strategic hedges

- Reduce exposure to long-duration USD-denominated debt

- Consider FX overlays to hedge dollar devaluation

- Monitor central bank gold flows as leading indicators of reserve regime change

VII. Dollar on the Precipice

The U.S. Dollar Index is resting precariously on long-term support dating back to 2011. A break below this trendline could trigger a sharp decline. Minor support from the July 1st bounce at 96.45 is vulnerable.

Political pressure on the Fed is intensifying. Trump and Bessent are pushing Powell to cut rates dramatically, citing housing and labor softness. But the labor force has shrunk by ~800,000 jobs — many undocumented — and hiring is frozen amid trade policy uncertainty. The Fed is further from its inflation target than its employment mandate.

VIII. Stocks are Struggling

After posting new all-time highs, stocks are struggling to make new gains. Normally, when a market makes a new all-time high, it is followed by a burst of fresh buying that pushes the market sharply higher prior to some exhaustion. In this case, the exhaustion set in early. The problem is that the algorithmic traders are already maximum long, and the value players are nervous about the market being dramatically overvalued. In an ideal trading scenario, Powell will confirm that the softening labor market warrants some action by the Fed. That will likely act as a catalyst to propel the market higher in a blow-off top. Then we can position ourselves for the inevitable reversal as bubble-like conditions become more and more apparent. For the time being, I remain long volatility and patiently waiting for the right time to start building a short position in the S&P500.

IX. Final Word

We remain positioned for dislocation, not complacency. Gold’s behavior is diagnostic — it reveals whether the Fed is losing control of the narrative and whether the dollar is still trusted as a store of value or merely tolerated as a medium of exchange.

“Gold’s rally isn’t a flight to safety — it’s a flight from monetary fiction.”

Wishing you strength and clarity in the trenches.

Andy Krieger

*************

Question from Hannah K. in Salt Lake City:

Dear Andy,

I enjoy reading your newsletter, but I am confused about something. You used to point out many mistakes that Jerome Powell was making as the Chairman of the Fed. Now you are generally supportive of him. Why the change? Is it just that you don’t like President Trump, so you automatically defend people he is attacking, or do you think he is making better policy decisions?

Hannah

Response to Hannah K

Dear Hannah,

Thank you for your note and thank you for being a subscriber. You pose a fair question. It is true that I was previously very critical of the policy making of Jerome Powell. He admittedly had a difficult job during COVID, but after flooding the system with more than $5,000,000,000,000.00 (Five Trillion Dollars) it seemed obvious that a good chunk of that money needed to be drained from the banks. Inflation was almost certain to rear its ugly head, so I was horrified when he fought against monetary tightening by claiming that the obvious inflationary pressures were “transitory.” Milton Friedman’s dictum that “inflation is always and everywhere a monetary phenomenon” still reverberates through central bank corridors. There were obvious reasons to be concerned that the huge monetary stimulus could lead to extensive, pervasive inflation. But in practice, especially post-2020, Friedman’s view was seen to be increasingly incomplete. Supply shocks such as COVID demonstrated how real-economy constraints (energy, food, logistics) can drive inflation independently of monetary policy. Powell therefore had both supply shocks and monetary shocks at work. Inflation was not going to be just a transitory phenomenon. Unfortunately, Powell was really late in recognizing this.

Powell ultimately, belatedly, took aggressive steps to rein in inflation. In my view, he could have done more and been more aggressive, but he has been trying to engineer a so-called soft landing. Severe damage was done due to his misreading of the economy, but I believe that he has been doing the best he can in a tricky environment. In any event, I believe strongly that an independent central bank is absolutely essential to the strength and stability of our nation. President Trump and Treasury Secretary Bessent’s browbeating, criticizing, and bullying of the Fed to cut interest rates is a very, very dangerous development, for all of us. The dollar – in fact, the very fabric of our economy – is absolutely reliant on a strong, independent central that can act without political interference. If our central bank loses that independence, you will see a terrifying collapse of global trust in our currency and our markets. I don’t need to agree with all of Powell’s decisions to absolutely respect and value the institution. Even more importantly, I have come to hold a very high respect for him as he demonstrated admirable integrity to withstand the constant, aggressive public attacks on his professionalism, his intelligence, and his efforts. My views about President Trump and Scott Bessent are irrelevant insofar as we have a Federal Reserve that is headed by people with high levels of knowledge, experience, and honor. I don’t mind mistakes – they’re part of being an imperfect species. But I do mind improper interference in the integrity of one of the most important institutions in the world.