Gold’s Nap Time, Yen’s Gym Time

September 30, 2025

Thoughts on the Market

This report outlines the rationale behind my decision to fully liquidate my gold positions and strategically reallocate a portion of the risk into bearish U.S. dollar structures, with a particular focus on the Japanese yen. It is still very, very early with the yen idea, so I am only recommending a light exposure at the current time. The decision is grounded in technical exhaustion, inter-market signals, macroeconomic uncertainty, and evolving central bank dynamics.

1. Gold Liquidation Rationale

Technical Exhaustion

Gold is extremely overbought across all major indicators:

- Monthly RSI readings nearing 90 – the highest level I have ever seen!!

- MACD divergence signaling waning momentum

- Bollinger Band expansion at historically unsustainable levels

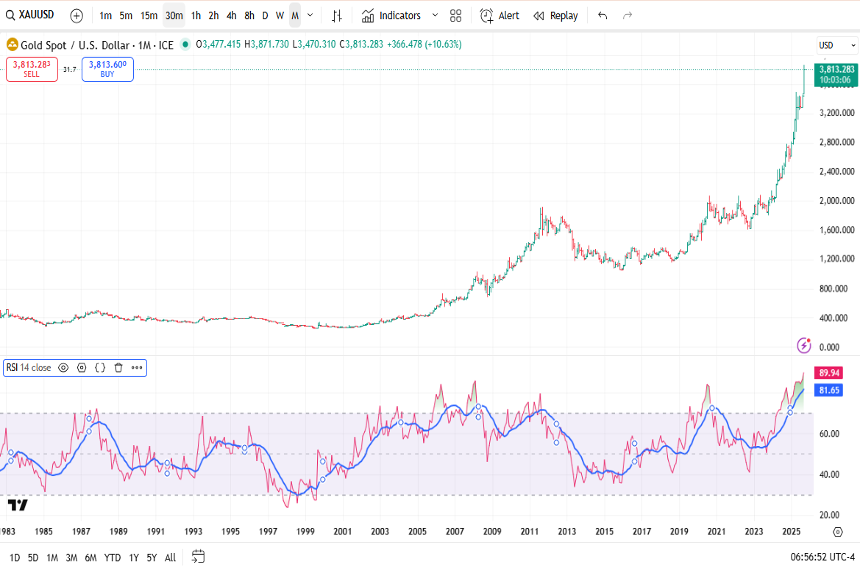

Price Target Achieved

After many months, gold has reached my long-term, stated target of $3,880 per oz, fulfilling the original thesis behind the position.

Inter-Market Signals

Silver’s explosive rally has brought it near all-time highs, but long-term charts show it is astonishingly overbought, suggesting potential exhaustion across the precious metals complex.

Macroeconomic Uncertainty

- Looming U.S. government shutdown

- Mixed economic data: weak employment and manufacturing vs. strong consumer spending

- Heightened volatility and policy ambiguity

2. Strategic Rotation: Bearish Dollar Structures

Oversold Yen and Rate Differentials

- The yen is deeply oversold against major currencies

- Japanese 10-year yields have surged over the past 2.5 years

- U.S. 10-year yields have stagnated or declined

- The narrowing spread undermines the yen carry trade, which is vulnerable to liquidation

Japan’s Economic Tailwinds

- Tourism boom and surging Nikkei index

- Massive foreign capital inflows

- Japan’s relative valuation is highly attractive, supporting currency revaluation

BOJ Policy Shift

- The Bank of Japan is signaling another potential rate hike at its October 29-30 meeting

- Hawkish sentiment is rising, with multiple board members advocating for tightening

- A rate hike would further compress global differentials and support yen strength

Fed Policy Vulnerability

- The Federal Reserve appears willing to let the economy run hot

- Persistent inflation above the 2% target is being downplayed

- Rate cuts are likely even amid data disruptions from a shutdown

- Fed officials have minimized tariff-driven inflation, signaling dovish bias

3. Portfolio Outlook

Post-liquidation, the portfolio is lighter now, with an initial light exposure toward:

- Bearish dollar structures, especially long yen exposure

- Reduced commodity risk, with gold and silver positions closed or minimized

- Opportunistic currency plays, targeting undervalued assets with macro tailwinds

This strategic pivot reflects disciplined risk management and a forward-looking view of global macro dynamics. By exiting overextended gold positions and beginning to enter undervalued currency structures, the portfolio is better positioned to navigate volatility and capitalize on asymmetric opportunities.

It should be quite clear from the charts below that Japanese 10-year rates have risen sharply over the past several years as inflation has finally become established in the Japanese economy. It took a major effort by the authorities over the past thirty-five years, but it appears that the crushing deflationary cycle in Japan has come to an end.

· Below is the chart of the 10-year Japanese government bond yield. It has clearly been trending higher for the past several years. In fact, the rise in yields has been quite dramatic. This move in rates is absolutely not priced into the yen’s relative performance in the forex markets. While speculators were aggressively selling yen when Japanese yields were much lower, they have not yet unwound their positions on the back of much higher yields. It is best to think of the yen’s reversal as an idea whose time may be coming. I am not fully on board the trade yet, but I am very, very interested in the idea. The unwind of exposures, when it comes, will be violent.

· At the same time, you can see in the chart of the U.S. 10-year government bond yields below that despite the somewhat wild fluctuations, the overall trend in interest rates for the past nine months has been lower. As you can easily see, the rate differential has narrowed very sharply!

· Below are several charts of gold and gold futures. As you can see, the market reached my long-term stated target of $3880 which triggered my decision to unwind our final exposure. Also, you can see from the RSI indicators how the gold market is very overbought and in need of a significant breather. It could come in the form of an extended period of broad consolidation, or perhaps a shorter-term sharp correction. In either case, I want to hit pause on my positions for the time being. This is significant, because it is the first time in many, many months that I want to sit on the sidelines. I have never seen gold so overbought on the monthly charts. Experience tells me that we should accept some profits and wait for the technical conditions to become more balanced. Eventually, the market will have more upside, but for now, I want to watch.

· In the monthly chart of spot gold below you can see the amazingly high RSI of this asset class. As noted, I have never seen such a reading before. This market is flashing bright warning signals to BE CAREFUL! Yes, I still like gold higher and expect it to rally further, but the market needs to digest its gains and find some balance before it can comfortably sustain much higher levels. Also, once a market reaches my long-term target (or comes very close to it), I have learned that it is prudent to exit the position and watch for a while.

· In the charts below, you can clearly see that silver has had a dramatic rally, and it also needs to take a pause. Silver is way overbought, and it will likely need to consolidate a bit before it has the power to take out the all-time highs on a sustained basis.

· Here you can see how close silver has come to its all-time peak. Frankly, after such a massive rally – over 100% in the past two years – it is time for the silver market to start correcting and consolidating as well. This doesn’t mean that it can’t go a bit higher first, but the risk-reward has now shifted sharply against a long position without a very, very tight stop-loss order. Given the close trading relationship between gold and silver, these numbers gave support to my decision to exit my gold position.

4. Tactical Extension: Short Canadian Dollar vs Japanese Yen

Building on the core thesis of yen appreciation beginning soon, I am also initiating a short position in the Canadian dollar versus the Japanese yen (CAD/JPY). This trade aligns with the same macro and technical logic driving my bearish dollar structures and long yen exposure.

Oversold Yen, Weakening Fundamentals in Canada

- The yen remains deeply oversold, not just against the U.S. dollar but also against commodity-linked currencies like the Canadian dollar.

- The Canadian dollar, buoyed somewhat by elevated energy prices and resilient domestic data, is now showing signs of technical exhaustion on long-term charts.

- CAD/JPY has rallied to levels that historically precede multi-week (and possibly, multi-month) reversals, with RSI and momentum indicators flashing overbought warnings.

Rate Differentials and Central Bank Divergence -- Canadian Economy: Recent Performance

- GDP Decline: Canada's economy contracted by approximately 1.5% in Q2 2025, largely due to trade uncertainty and the impact of tariffs. Exports fell sharply by 27%, reversing gains from Q1.

- Employment Weakness: The labor market has deteriorated, with 66,000 jobs lost in August alone. The unemployment rate rose to 7.1%, its highest level since March.

- Business Investment: Investment declined in Q2, reflecting weak hiring intentions and trade-sensitive sector stress.

- Consumer Activity: Consumption and housing activity remained relatively healthy, but slow population growth and labor market weakness are expected to weigh on spending going forward.

- Inflation Trends: Headline CPI inflation was 1.9% in August, below the Bank’s 2% target. Core inflation measures hovered around 2.5–3%, but upward momentum has faded.

Bank of Canada: Rate Decision

- On September 17, 2025, the Bank of Canada cut its policy rate by 25 basis points to 2.5%, marking its lowest level since July 20222.

- This move ended a six-month pause and was driven by weakening economic data, especially labor market deterioration and soft inflation.

- The Bank cited reduced upside inflation risk and the need to balance economic risks as justification for the cut.

- The decision leaves the door open for further rate cuts, with upcoming meetings on October 29 and December 10 being closely watched.

Against this backdrop of softening rates in Canada, we have the Bank of Japan nearing a rate hike (currently about a 70% probability). While the Bank of Canada has signaled a pause amid mixed economic signals, the interest rate differential has already narrowed significantly, but the currency markets don’t yet reflect this narrowing.

- As Japan tightens and Canada stalls, the interest rate differential narrows further, undermining the rationale for long CAD/short JPY carry trades.

- This setup mirrors the dynamic seen in USD/JPY, where entrenched carry positions are vulnerable to unwind.

Macro Tailwinds for the Yen

- Japan’s improving fundamentals — surging tourism, strong equity performance, and foreign capital inflows — support a broader yen revaluation.

- The CAD, by contrast, faces headwinds from slowing global demand, potential oil price volatility, and domestic housing market fragility.

Strategic Implication

- Short CAD/JPY offers a diversified expression of yen strength, reducing reliance on USD-specific catalysts.

- It also provides exposure to a commodity-vs-consumer economy divergence, with Japan benefiting from global disinflation while Canada remains tethered to cyclical commodity flows.

Please note that I have not initiated heavy long yen exposures yet. I will increase the exposures once the market starts to provide clearer confirmation that the trends are underway. It is always a bit dangerous to play for reversals, so I advise either limited risk option strategies or very light spot positions with trailing stops.

In my next write-up I will address some of my targets in the yen and yen crosses. I will also share some thoughts about the U.S. economy and the S&P500, although these are tricky topics. In the meanwhile, I want to wish you all the best of luck with your trading, and I hope that you were able to enjoy the sustained gold rally along with me and my team

Andy Krieger