How We Are Adapting Our Trading to the Ever-shifting Policies from Washington

Thoughts on the Market

March 2, 2026

Over the past thirty-four years I have stayed clear of politics in my writings. Whether I was writing publicly for Forbes, in my book, or privately for my investment clients, I have tried to maintain a strict policy by which my writings should focus on an analysis of market trends and market dynamics rather than judging or choosing sides in the never-ending game of political drama. That doesn’t mean that I am not keenly aware of governmental policies; I follow both fiscal and monetary policies very closely as they play an important role in my financial analysis. To the extent I have strayed from my neutral stance, it was typically when I lambasted Federal Reserve monetary policy that was grotesquely inconsistent with the Fed’s legal mandate as set forth in the Federal Reserve Act of 1913.

Specifically, the Federal Reserve’s legal mandate is to promote maximum employment and stable prices. The Fed’s policy is supposed to be geared towards promoting non-inflationary growth, and it has clearly missed the mark more than a few times. I have been particularly vocal about Jerome Powell’s bungling of monetary policy and misreading the economy’s obvious inflationary pressures; especially after covid when he made his unfortunate comments about inflation being transitory. At the same time, I have also noted how Powell has earned my respect by handling the shocking level of personal abuse from the president in a professional and dignified manner. But since Powell is not an elected politician, I felt few constraints in attacking his policies.

I am writing about this because I have remained silent during seven presidencies, but I have to confess that President Trump is sorely testing my convictions. Trump 2.0 has been nothing less than remarkable in many ways. (Please note that the word “remarkable” does not necessarily imply “good”). Perhaps the words of the Supreme Court’s Chief Justice, John Roberts, in his ruling on Trump’s tariffs best summarizes my views. Let me put this into context:

(Please allow me to interrupt with a bit of housekeeping: To those of you who are still thinking of subscribing, this is the week to do it, as our pricing model will change as of March 10th. To my esteemed current subscribers, have no fear: your rate is grandfathered.)

Roberts explained why, as a matter of statutory interpretation and the constitutional separation of powers, President Trump lacked the authority he had claimed – theoretically under the International Emergency Economic Powers Act – to impose a hodgepodge of tariffs on countries all over the world. Roberts, however, in a highly unusual move, deviated from his normal practice of exclusively sticking to the law and legal opinion and wrote the following paragraph, summarizing in condensed form some of the chaos associated with Trump’s usage of tariffs.

“Since imposing each set of tariffs, the president has issued several increases, reductions and other modifications. One month after imposing the 10 percent drug trafficking tariffs on Chinese goods, he increased the rate to 20 percent. One month later, he removed a statutory exemption for Chinese goods under $800. Less than a week after imposing the reciprocal tariffs, the president increased the rate on Chinese goods from 34 percent to 84 percent. The very next day, he increased the rate further still, to 125 percent. This brought the total effective tariff rate on most Chinese goods to 145 percent. The president has also shifted sets of goods into and out of the reciprocal tariff framework ([e.g.,] exempting from reciprocal tariffs beef, fruits, coffee, tea, spices and some fertilizers). And he has issued a variety of other adjustments ([e.g.,] extending ‘the suspension of heightened reciprocal tariffs’ on Chinese imports).”

From the perspective of the Supreme Court and as a matter of law, the sensibility of tariffs doesn’t matter. It truly doesn’t make any difference whether they were imposed arbitrarily or with great care and analytical precision. The point that Roberts is making is that we now have a president who is capricious and volatile, and the president is sowing chaos in America and around the globe. In fact, Roberts could have carried on for quite a few additional paragraphs about the chaos associated with Trump’s tariffs, but his point was clear.

The fact that the president then called John Roberts, the Chief Justice of the highest court in the land, “a lap dog” and “a fool who is swayed by foreign interests” pretty much proves the point that Roberts is making. We have rarely had a president who behaves (at least in public) like this, and we need to be acutely sensitive to this fact when we are making investment decisions. Unlike certain domestic policies which are getting a lot of headlines in the U.S. press, tariffs are explicitly and directly key factors in global trade and finance, so I feel that it is ok to write about them.

I warned my readers over a year ago that Trump 2.0 was going to be wild and highly unpredictable, but I clearly missed the mark because I severely underestimated just how unpredictable Trump 2.0 was going to be. But opportunity comes where you least expect it: reflecting back, it is the unprecedented unpredictability of the current administration that led to my design of a trading strategy that is uncannily well-suited to Trump’s chaotic policy-making. Let me explain.

Since 1984, I have traded options professionally, using a variety of strategies that matched my specific macro views. For example, in the mid-1980’s, the U.S. dollar’s decline was obvious and highly predictable. When the currencies started floating freely in 1973, the exchange rates were extremely mispriced. The dollar was tremendously overvalued, and it was going to take many years before the rates could settle into more appropriate ranges.

Consider the path of USD/CHF:

-Fixed USD/CHF rate in early 1971: ~4.375 CHF per USD

-Revised fixed rate after December 1971: ~4.05–4.10 CHF per USD

-Floating begins in 1973: ~3.8–3.9 CHF per USD

-Currently trading at .78 CHF per USD

The dollar had a similar path against the yen:

-Pre-1971, Dollar/Yen was fixed at 360 yen per dollar.

-The yen was then revalued to 308 yen per dollar before the free float in1973, when USD/JPY traded at 280 yen per dollar.

-After the free float, the dollar continued to decline, with periodic help from the authorities who were intent to driving the dollar down to more sustainable levels.

-Currently trading at 157.50 yen per USD (having traded as low as 76.00 yen per USD

Through the 1980’s and 1990’s, there was little doubt about the primary trends in the forex markets. Dollar bearish directional plays were obvious and quite easy to structure.

There were also many obvious directional plays in the 1990’s due to macro events such as German unification and the British pound’s subsequent collapse against the Deutsche Mark (and other currencies).

Why the pound was vulnerable in the first place

The crisis was inevitable because the UK had locked itself into an exchange rate that didn’t match its economic fundamentals:

- High inflation relative to Germany

- A recession and weak domestic economy

- German interest rates rising after reunification, forcing the UK to follow rates that were too high for its own economy

- An ERM entry rate (£1 = 2.95 DM) widely seen as unrealistic

This created a structural contradiction: the UK needed lower interest rates to support growth, but ERM rules required higher rates to defend the currency.

My bias was to always be net long options, and the trends allowed my strategies to work beautifully. There have been many macro events over the past forty years which have made directional plays in forex and other markets very rewarding. Whether it was the bursting of the Dot-Com bubble or the Great Financial Crisis, we have had plenty of exciting opportunities that were fairly predictable. What we haven’t had until now is a regime that is typified by consistent unpredictability.

We have a president who ran on the promise that we would not interfere and get involved in international military conflicts. Trump’s campaign messaging on international military conflicts centered on presenting himself as a non‑interventionist “peacemaker” who would end wars rather than start new ones. The key themes of his promises can be grouped into three areas: ending “forever wars,” avoiding new entanglements, and using strength as deterrence.

Core campaign promises about military involvement

Trump repeatedly framed U.S. military intervention as wasteful, misguided, or contrary to American interests. Across his campaigns, several consistent themes emerged:

Ending “forever wars”

Trump frequently promised to end long-running U.S. military engagements, especially in the Middle East. He worked hard to cast himself as a leader who would stop global conflicts and bring troops home.

Positioning himself as a “peacemaker”

He described himself as someone uniquely capable of brokering peace and resolving conflicts quickly. For example, Trump claimed he could end the Russia‑Ukraine war “within 24 hours,” a signature line of his campaign rhetoric.

“America First” non‑interventionism

Trump’s broader foreign‑policy message emphasized avoiding unnecessary foreign entanglements and prioritizing U.S. interests over global commitments. This included skepticism toward large-scale military efforts to support nation-building efforts or regime change.

How he contrasted himself with past U.S. policy

On the campaign trail, Trump repeatedly said:

- Prior administrations had dragged the U.S. into costly, endless conflicts.

- The U.S. should not act as the world’s policeman.

- Military force should be used only when absolutely necessary and only in ways that directly benefit the U.S.

It is with these promises in mind that I have found his capture of Maduro and the recent attacks against Iran more than a little surprising. Did I like how Maduro ran Venezuela? Absolutely not – many Venezuelan people were truly suffering under his regime. Do I like the policies of the ruling regime in Iran? No. I abhor the Iranian government’s treatment of women in general, and their cruel punishment – and too often, killing – of any citizen who chooses to speak their mind. Therefore, I am not judging the intentionality of Trump’s decisions. Rather, I am simply noting that these actions further support my contention that he is highly unpredictable.

His recent decision to attack Iran to bring down the Iranian government has triggered a violent reaction in the commodities markets and has generated some exceptional short-term volatility in equities and currencies. Actions creating this sort of market reaction are what I have come to expect from the current administration, and the further refinement of my options strategies is a direct response to this unpredictability. Put differently, in the current political environment, I feel very confident taking well-defined positions in stock index options that are bets about the magnitude of moves over the next thirty to thirty-five days, rather than structural trend-following bets.

I believe that my job as a trader is to adapt and adjust to shifting market conditions, but in the current policy environment, it is a bit tricky to identify medium-term trends on an ongoing basis. Quite frankly, it is increasingly difficult to know what policy shifts might be coming next. Therefore, I feel very comfortable taking positions that bet on short-term movements which might last for a few days, or otherwise betting on the likely magnitude of moves over the next thirty or thirty-five days.

By way of further background, here is a list of the events over the past century that caused the most dramatic movements over a short period of time. We have used them as benchmarks to make sure that what we are doing now would have been safe in all of these environments.

-2020 COVID Crash

-2008 Global Financial Crisis

-1987 Crash

-1973–74 Oil Crisis

-1929–1932 Great Depression period

We are primarily trading the options on the S&P500, and our research indicates that the most severe movement during any thirty-five-day period over the past century actually occurred during COVID. In fact, during COVID the S&P500 dropped about 35% from peak-to-trough over a thirty-five-day period, so we use that drop as our benchmark to make sure our strategy is safe. Structuring a portfolio that will make lots of money safely while assuming the market can drop by 35% during a thirty-five-day period has been challenging, but ultimately quite rewarding. The probability of the market having a move that extreme is exceedingly low, but our portfolio assumes it is always possible.

We are not oblivious to the fact that the market might have an even more extreme move at some point, and we have found some ways to layer in quite inexpensive protection in case the next wild move proves to be even larger than the 2020 COVID crash. If you are fascinated by probabilities and numbers, you should plug in the data from these moves and determine the probability of future moves of this magnitude occurring. I can assure you that these are very low probability events that might be matched (or even exceeded) at some point – but only very rarely.

Our revamped approach has resulted in a strangely relaxing feeling with our trading – it's a feeling that I've never had before. In fact, Imre and I find it so relaxing that it sometimes feels a bit unsettling. We don’t believe in selling options naked, but we have devised a variety of strategies that enable us to generate very attractive premium while still owning lots of options that can generate outsized returns over very wide trading bands. Is this strategy 100% guaranteed to generate profits? Of course not. We do, however, try to build portfolios that will hold up under nearly every condition and run rigorous stress tests assuming extreme levels of volatility, but since markets have fat tail distributions, we can’t guarantee success. On the other hand, we have been able to generate profits for each of the past seventeen months, so we’ve either been extraordinarily lucky … or the strategies we are using are remarkably sound.

Our original strategy has morphed and evolved as Trump has layered in progressively more and more uncertainty into his policy formation. The unfortunate thing is that I prefer to use option strategies as a vehicle to capture major market swings, but for the time being we will play the hand we’ve been dealt and continue to focus on strategies that we know are tried-and-true in the current environment.

That said, I want to point out again how lucky we all are to have Imre Gams contributing to these newsletters. For short-term technical analysis, I don’t think you will find anyone better than Imre. Please read his write-up carefully. There is a lot you can learn from him.

Next week, I will provide a variety of forecasts, trade ideas, and market updates, but I wanted to use today's newsletter to share these thoughts about how we are handling the chaotic policy shifts of the current administration.

Andy Krieger

*****************************

From Imre --

I am thrilled to announce that my episode on the world’s largest trading podcast, Words of Rizdom, is now live.

You can check out the full interview here -- https://www.youtube.com/watch?si=hDGBRQvAsH5MHN7O&v=vpgIcxHV1tw&feature=youtu.be

My Framework:

I treat markets as auctions, not prediction machines.

Most sessions on a day-to-day basis are balanced.

Edges form at the extremes of value.

I trade acceptance and rejection at those edges.

If value migrates, I align with it.

If it fails, I trade the rotation.

I am not in the business of forecasting.

I am in the business of validating participation.

_________________________________________________________

Last week’s analysis was a textbook example of rotational trading in a balanced regime.

Balanced or sideways markets are only as challenging as you make them to be.

Applying trending or breakout strategies to a balanced regime is the definition of structural inefficiency.

Mean reverting and rotational strategies are far more structurally efficient.

This is why I wrote that my best trades on ES will come from the structural edges of value.

Specifically buying from 6817 and selling from 6973.

Last week’s high was 6983.

As for this upcoming week, traders can certainly expect movement across all major markets.

The concentrated armed conflict in Iran has sent shockwaves around the world.

President Trump has confirmed rumors that Ayatollah Ali Khamenei has been eliminated. It

remains to be seen whether his death will bring an immediate end to the war.

Disruptions to the Strait of Hormuz will be a critical point of focus for the markets.

My approach to factoring geopolitical events with my technical analysis is to acknowledge events as potential volatility catalysts.

Beyond that, I do not associate any kind of predictive property with the news. Regardless of what that news may be.

We will start this week’s analysis with ES.

The parameters for ES remain the same. The market is still in a balanced regime.

The value area is still 6973.50 and the value area low is 6817.50.

Until we can observe acceptance outside of the value area, rotational mean-reverting trades from the value area extremes remain the highest-probability setups.

A strong market will accept fair value above 6973.50, signaling a further push to new all-time-highs.

A weak market will accept fair value below 6817.50, opening the door for a test of 6770. The next major downside target would be 6700.

Next, we will move on to Gold.

In previous analysis, the key level for gold traders was 5100.

This past week marked acceptance above this key level.

In the screenshot below, I have highlighted what this acceptance looks like. Take careful note of two clear failed auctions that attempted to initiate re-pricing both below and above the accepted range.

But it is critical to note that acceptance does not imply continuation. All it means is that the market is accepting this range as new fair value.

In order for continuation higher, the market must be able to continue migrating acceptance higher as well. Continuation requires initiative plus structural reinforcement.

Continuation higher would require three things:

1. Initiative participation

Aggressive buyers lifting the offer.

Not passive drifting.

Not thin liquidity pops.

Real urgency.

2. Opposing passive liquidity failing

Sellers sitting on the offer either get absorbed or step away.

If they reload and cap price, you are still in balance.

If they get overwhelmed, the auction shifts.

3. Supporting passive liquidity advancing

Buyers raise bids.

They defend prior structural references.

The bid does not collapse back into the range.

A successful breakout higher should see buyers targeting the previous all-time-high in gold and beyond.

A failure to remain above the key 5100 level would see a rotation back toward approximately 5030 to 5000.

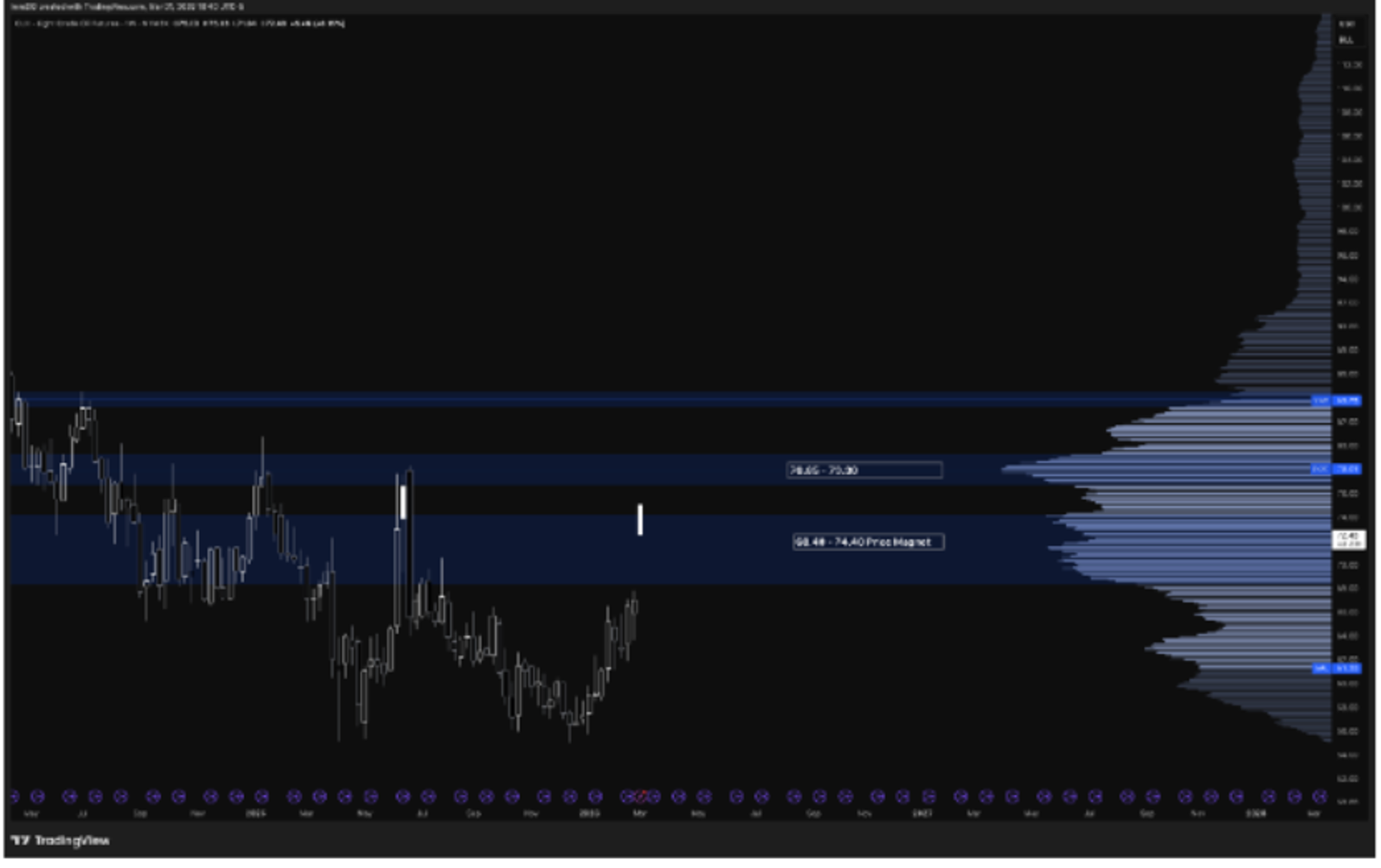

Our final market in focus will be Light Crude Oil futures (CL).

Given the ongoing geopolitical tension in the Middle East, CL is certain to experience heightened volatility.

Increases in volatility can make for fantastic trading environments, but such environments also warrant extreme caution.

This week I am keeping a very close eye on two major distributions in CL. The first is a range between 68.40-74.40.

On Sunday evening’s market open, CL gapped up over this range before quickly getting sucked back into it.

A weak market will be unable to sustain this peek above the range.

Trading back towards the bottom of this range would also result in much of the gap up being filled.

In the event of the gap being filled, it will be interesting to see if buyers are willing to step in and defend the 68 level, potentially resulting in a fresh rotation back toward the top of the range at 74.40.

Holding above this distribution, however, means its upper value of 74.40 could hold as support.

A strong market would then target the next significant distribution spanning 76.85 to 79.30.