Major Storms Are Brewing

The market is behaving like all is good with the world... Few things could be further from the truth.

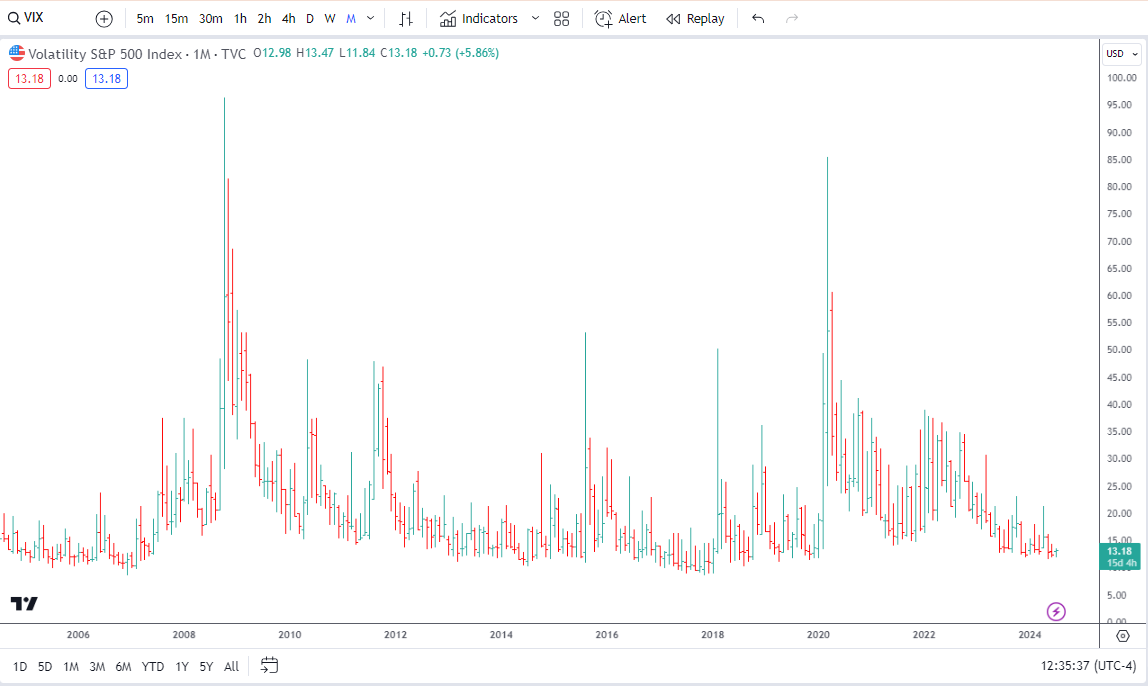

The chart above shows the S&P500 volatility over the past eighteen years. The chart since 1990 doesn’t look a whole lot different. The volatility of the stock market tends to revert to certain basic patterns. The bottom of the long-term range tends to stabilize between 11% and 13% annualized volatility, and the periodic spikes nearly always top out between 35% and 40%. Typically, after several years of basing around the lower volatility levels, spikes in volatility follow.

The extreme meltdowns in equities during the Great Recession and during Covid saw incredible spikes above 80%, and even above 90%, but those were unusual. Prior panics such as what we experienced during the bursting of the Dot-com bubble and during the Russian debt crisis and Long-Term Capital collapse were more typical, reaching about 40%.

For a variety of reasons, we need to prepare ourselves for volatility levels that will, at a minimum, approach those of the Dot-com levels.