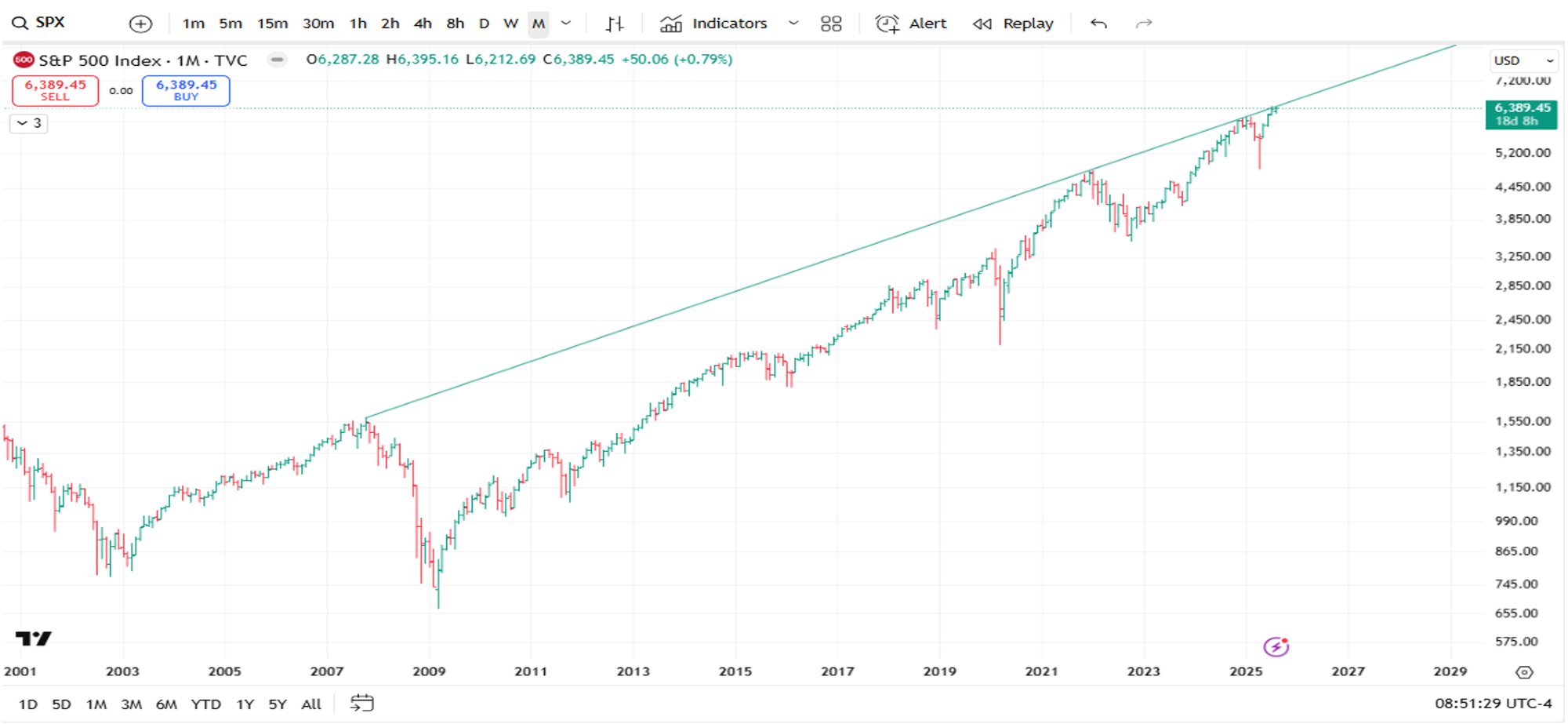

Market Crossroads: Preparing for the Final Blast

For some time now, we've anticipated one final surge in equities before a potential sharp correction and reversal. As the market tests major trendline resistance dating back to 2007, the next move will likely be dramatic. These moves will present excellent money-making opportunities, so we really need to pay extra close attention to the markets over the coming weeks. Even in markets like these, there are techniques that can help you mitigate downside risk and amplify profits. In the coming weeks, I will start to provide some examples of some of these techniques that are worth considering.

Two Scenarios, One Outcome: Volatility Wins

The chart below makes one thing clear: a steady grind higher is the least likely path. We're looking at two possibilities:

• A near-vertical breakout through resistance

• A sharp reversal and decline

Our bias leans toward a hybrid: an initial blast higher followed by a massive downturn. Either way, our long volatility exposure is well-positioned to benefit from sharp moves in either direction. We particularly like the idea of being long volatility when the VIX is trading at heavily compressed levels.

Portfolio Strategy: Time Decay and Tail Risk Protection

We continue to structure our portfolio with:

• Short-dated option spreads to earn time decay

• Long volatility plays for protection and excellent profit potential form sustained moves.

• Deep out-of-the-money puts as insurance against historic declines.

Violent market moves tend to skew downward, so we’re comfortable allocating a small portion of our returns to hedge against a long-term crash scenario.

Momentum vs. Discretion: A Divided Market

• Algorithmic traders are heavily long, with trend-following signals triggering aggressive buying – more so than at any time in the past five years.

• Discretionary traders remain cautious, citing economic uncertainty and overvaluation. Over 90% believe the market is overpriced.

This divergence sets the stage for maximum pain – something markets excel at delivering.

The Pain Trade: Blow-Off Top, Then Collapse

Markets often punish the largest number of participants with the greatest amount of suffering. A blow-off top would force reluctant investors to chase the rally, only to be subsequently crushed by a sudden reversal. As selling accelerates, both systematic and discretionary traders would be caught in a stampede for the exits.

Our proprietary systems suggest that medium-term trend followers won’t currently exit unless the S&P500 breaks below 6100. However, that threshold would rise if we accelerate higher – creating a perfect storm where the exit trigger hovers near current levels. The subsequent reversal after the market surge would then leave a vast number of speculators wounded and writhing in pain

Fed Watch: Rate Cuts on the Horizon?

Last week’s labor data sparked a seismic shift in Fed sentiment. Multiple officials now see labor market weakness as a greater risk than inflation, with some advocating for immediate rate cuts – even at the cost of higher inflation. Of course, this is typical thinking for our central bank, which has flooded our economy with excess liquidity for decades.

Investors responded by buying stocks, betting on Fed stimulus to boost earnings. But this isn’t a typical environment:

• The Fed is closer to maximum employment than its 2% inflation target• Tariffs are pushing inflation higher, not lower

Bad News Isn’t Always Good News

• While rate cuts often fuel rallies, today’s backdrop is more complex.

Inflationary pressures and policy uncertainty mean that speculators may not get the easy win they’re hoping for. If stagflationary conditions get really ugly, then we need to start thinking about how far a market decline might go. Have a look at the following chart.

Resistance Meets Support: A Tense Setup

In this chart, we can see the flip-side of the S&P500 trendline overhead resistance, which is a multi-year trendline which has provided powerful support for every major sell-off since Covid. Is it coincidence that the Liberation Day sell-off stopped exactly where the trendline came in? Is it a coincidence that the 4800 low in April happened to be not only where the supporting trendline came in but also happened to match the high point in January of 2022 – which also happened to be where the trendline resistance capped the rally? Are the trendlines causes or effects – or merely coincidental?

We can explore the philosophical aspects of this another time. The important thing here is to understand that if things turn ugly enough for the market to have the power to slice through the multi-year trendline support, then we need to brace ourselves for a further collapse of historic proportions.

In any case, our long volatility bias coupled with our extra out-of-the-money puts will enable us to capitalize handsomely if we break below this support and cascade lower.

Turning briefly to currencies, I want to note that we are approaching critical levels there as well. I will write about forex in greater detail next week, but in the meantime, here is a question that was asked by one of our readers, followed by my answer:

From John S. in Kuala Lumpur

Question:

"Andy, you have written a lot about the coming crisis for the US due to the mounting debt. You are also quite bearish on the US dollar versus the other major currencies. Given the fact the US has higher interest rates and an economy that is doing so much better than the economies in Europe and Japan, why are you bearish on the dollar. It seems it should be going higher, not lower."

Answer:

"John, you have raised some good points. It is true that the US economy is outperforming the economies in Europe and Japan. It is also true that the US interest rates are much higher than the rates in Europe and Japan. I could go into many technical reasons for the dollar to break down, but let's consider the following:

1. Germany, is finally going to start borrowing and spending massive amounts of money to boost their economy. I wish they weren't doing it because of pressure to boost defense spending, but extra spending will provide huge support to their economy. They have been very cautious for a very long time to increase their debt, so this is a major shift.

2. Japan is finally breaking out of 35 years of a de facto sleeping economy. They have the early shoots of sustained inflation, and they will continue raise rates – finally. They will do it slowly and methodically, but the shift is underway.

3. The Fed is going to start cutting rates – perhaps aggressively. They will likely ignore the inflation in the economy and pretend it isn't there. This will likely fuel an ever-greater bubble in stocks, but the lower rates will force more unwinding of carry plays.

4. The ECB and Bank of England have already cut rates a lot, and they are less likely to keep cutting. For sure the US has more room to cut than the other countries.

5. Long term – the US debt situation will create even bigger, more structural problems, but for now, we can focus on the expected narrowing differential between US and foreign rates, major fiscal shifts in Europe (finally borrowing and spending to boost extra growth), and a broader global reallocation of assets away from the US to participate in other stock market opportunities. On a relative basis, US stocks still comprise way too big a percentage of global asset allocations."

Currency Watch: Dollar on the Edge

The dollar is barely holding key support. If conditions deteriorate, we could see a violent move lower in the dollar over the coming months.

• A weaker dollar may help address trade deficits, but structural imbalances remain.

• The U.S. imports goods it cannot competitively produce and runs persistent service surpluses. Unfortunately for our trade partners, Trump refused to recognize our service surpluses as being relevant.

• Tariffs and currency moves won’t erase these dynamics.

Trump’s disproportionate tariff deals were enabled by America’s military role -- not economic leverage. The dollar’s July rally has neutralized speculative shorts, leaving the downside wide open.

We expect a modest 4% to 5% drop in the near term -- but over the next year, something far more violent may unfold.

Final Thought

Volatility is quiet. Too quiet. This is the calm before the storm in stocks and currencies. I feel strongly that the recent compression in the market presents a wonderful trading opportunity. Volatility in the S&P500 is trading at or near its lowest level in many months (see the chart below). Historically, this sort of compression rarely lasts more than a few months. As noted, we need to pay extra close attention to the markets as this sort of compression is nearly always followed by an explosive move. There are lots of ways to structure attractive risk-reward trades in pretty much any market scenario, and I will be addressing these sorts of opportunities in great detail in my small group classes. My bias is to use long option strategies in the current environment, but I recognize that not all of you have a lot of experience with options. Once the move develops, then we will be able to structure excellent trades just using futures with sensible stop-loss orders. Overall, the markets appear to be a lot calmer than usual, but don’t be deceived. The current calm in the markets is not sustainable.

We remain positioned for dislocation, not complacency. In the meanwhile, I am wishing you all the best of luck in the trenches.