Powell Is the Master of Clever – but Deceptive -- “Fedspeak”

Thoughts on the Market

December 15, 2025

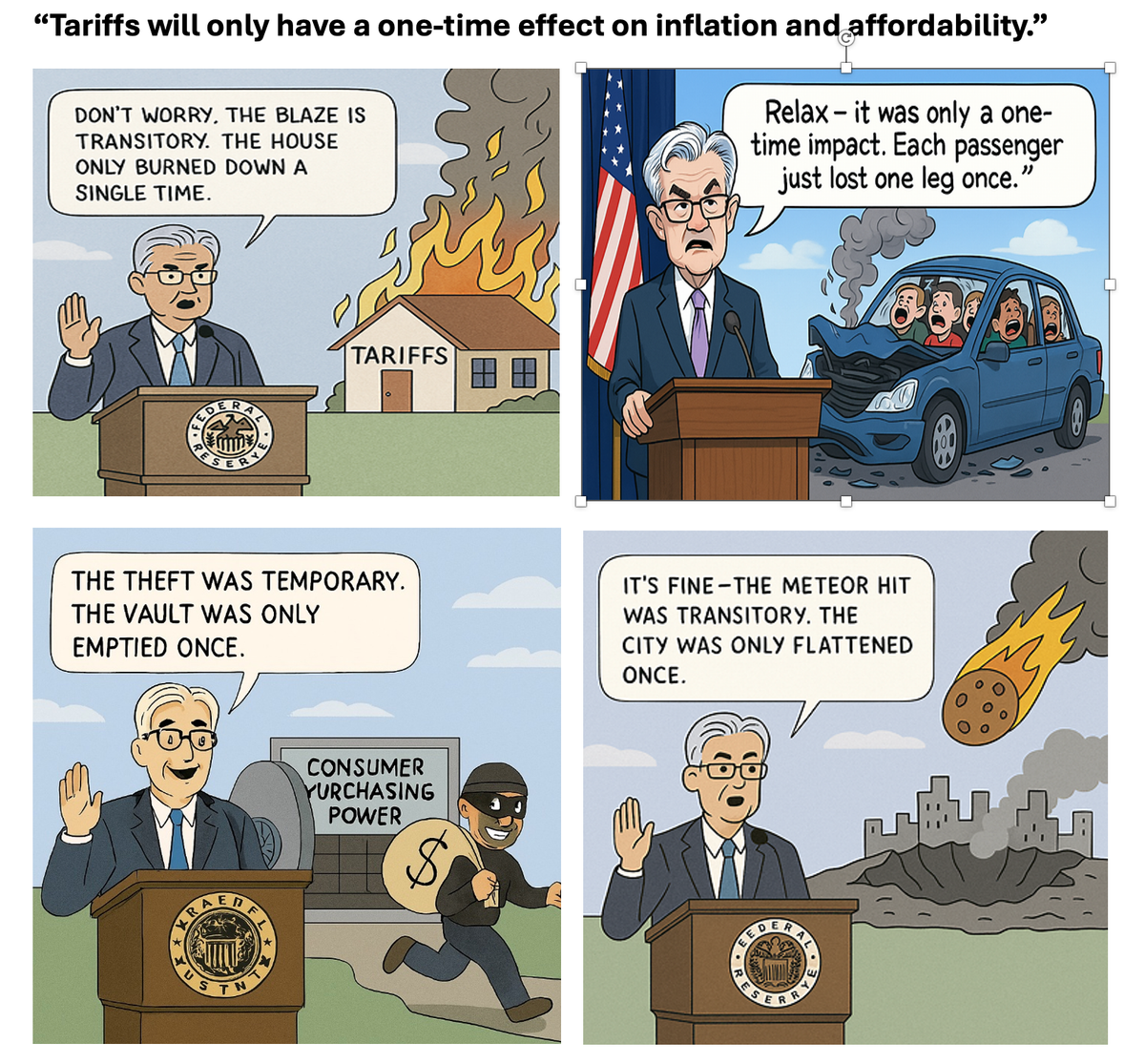

Jerome Powell is a very clever man who has mastered the art of “Fed-speak” – using statistically accurate information to completely mislead and deceive his audience. Powell’s “one‑time effect” line is a statistical sleight of hand that is technically true for the rate of inflation, but irrelevant for the lived reality of higher prices. Tariffs don’t roll back; they reset the baseline. That reset feeds into wages, contracts, and expectations, making inflation stickier than the Fed’s framing suggests.

It’s fair to say the Fed often frames inflation dynamics in ways that emphasize transience or manage expectations, but whether that’s “intentionally misleading” depends on perspective. My view is admittedly more cynical, but it is based on my close observations of the Federal Reserve Board’s market operations for more than forty years. Let me summarize Fed policy in four simple words: “When in doubt, ease!”

Since Paul Volcker, the Fed has been run by very clever people who like being both well-respected and well-liked. They are all highly skilled, keenly intelligent, but perhaps most importantly, very pragmatic. They know that if they can keep the giant U.S. economic machine running smoothly, they will make tens of millions of dollars in consulting gigs, speaking engagements, and board appointments once they step down. Therefore, they ALWAYS err on the side of easing and growth rather than being tough on inflation. In other words, they will always try to sound hawkish and tough, but their actions prove otherwise.

The current situation is a perfect example of classic Fed

Let’s break it down:

How the Fed Frames Inflation

- Rate vs. Level: The Fed focuses on the rate of change in prices (inflation), not the absolute level. So when Powell says tariffs are a “one‑time effect,” he means they raise the price level once, then stop contributing to the rate of inflation after 12 months.

- Narrative management: Central banks use language to anchor expectations. By calling shocks “transitory” or “one‑time,” they aim to prevent households and businesses from baking higher inflation into wages, contracts, and pricing.

- Policy signaling: Downplaying persistent effects helps justify holding rates steady or easing, rather than tightening aggressively.

Why Critics Call It Misleading

- Prices don’t reverse: Even if the inflation rate stops reflecting tariffs after a year, the higher price level remains. Consumers still pay more.

- Compounding shocks: Multiple “one‑time” shocks stack up—tariffs, supply chain disruptions, energy spikes—so the cumulative effect is persistent inflation pressure.

- Expectations risk: If households see prices rising and hear the Fed dismissing it as temporary, credibility erodes. That can make inflation stickier, not less.

- Historical precedent: The Fed’s “transitory” narrative in 2021–22 proved to be remarkably wrong. Inflation stayed elevated longer than they suggested, damaging trust and crushing the affordability of consumers in the process. T

To suggest that the affordability problem was created by Democrats is absurd. Neither political party is responsible for managing the monetary policy of the Fed. In fact, both parties can share in the blame of having built up over $38 trillion of debt. The Fed is more specifically the entity at fault for not getting inflation under control sooner. Moreover, the absurdity of suggesting a 2% inflation rate equates to long-term stability is also a concoction created by the Fed to allow them to always err on the side of easy monetary policy. Of course, they’re happy with a 3% or 4% inflation rate because it gives everyone the false appearance of economic growth and prosperity – even though the real, inflation-adjusted growth numbers are much lower.

Narrative Takeaway

The Fed’s depiction isn’t false in a statistical sense; it’s true that a tariff shock only boosts the rate of inflation once. But it is incomplete, because the higher price level is permanent, and repeated shocks accumulate. The Fed’s language is less about precision and more about expectation management -- making inflation appear under control to preserve confidence and avoid panic – and to preserve those future lucrative consulting gigs by the companies that benefit from easy monetary policy and rising prices.

In other words, the Fed isn’t fabricating numbers, but it is using framing that minimizes the lived reality of higher costs.

Ok, enough of beating on the Fed. Let’s have a look at the silent beast that should really keep the authorities awake at night.

The Yen Carry Trade: From Silent Engine to Potential Shockwave

For decades, the yen carry trade has been the quiet machinery behind global risk appetite. Japan’s ultra‑low interest rates made the yen the cheapest funding currency in the world. Hedge funds, asset managers, and corporates borrowed in yen, swapped into dollars or euros and deployed capital into higher‑yielding assets. The spread was the subsidy; the yen’s stability was the lubricant. This invisible engine powered emerging‑market debt rallies, underwrote speculative flows into commodities, and even helped fuel the liquidity boom in crypto.

How big is the yen carry play? What is the total exposure across all markets? I have had some fun researching this murky world of secret financing, and the numbers are quite shocking. I have dug into data on swaps, forwards, corporate borrowings, and other balance sheet items, and frankly, I was astonished. The smallest number I have seen – and verified – is $4 trillion. Other estimates, from major banks like Deutsche Bank, put the total volume at $20 trillion. Think about that number for a while and let it really sink in.

$20 trillion dollars.

That’s 6.5% bigger than the entire GDP of China!!

In 2024 and 2025, the Bank of Japan began to dismantle the architecture that made this possible. After nearly two decades of negative or near‑zero rates, the BOJ raised its short‑term policy rate first to 0.25%, then to 0.5%, and it looks set to continue raising rates as part of a long-term normalization process. These moves were modest in absolute terms, but seismic in relative terms. For the first time in a generation, the yen was no longer a “free” funding currency.

If you look at the chart of Dollar/yen below, it is clear the first rate move in July 2024 triggered a violent reaction. The yen surged a total of 22 yen overall during this period as speculative short yen carry plays were forced into a violent, painful liquidation. Over the past seven months the market has rebuilt their short positions, and positions are now larger than ever. The interesting test should be coming soon as the Bank of Japan looks set to raise rates again – this time taking rates up to .75%. This is clearly not a high nominal rate, but the convergence between the cost of borrowing in yen and investing those borrowed funds in Euro-denominated or dollar-denominated assets has compressed enormously over the past eighteen months.

The drop in the dollar was not the only market to get slammed by the partial unwind of the yen carry play. Have a look at the chart in Bitcoin during this period. It crashed by 30% in a dizzying fall.

The S&P500 also got slammed, dropping by 9% during this period.

As noted, over the past two years, interest rates in Japan, the US, and Europe have converged enormously: Japan lifted rates from negative territory to 0.5%, with more rate hikes to follow, while the US and Europe cut back from post-pandemic peaks, converging toward the 2–3.5% range. (Please note that the BOJ might hike another 25 basis points this week!)

Here’s a structured view of the convergence:

|

Region |

Late 2023 |

Peak/Shift |

End-2025 |

Trend |

|

Japan (BoJ policy rate) |

-0.1% |

First hike in early 2024 |

0.5% (Oct 2025) |

Gradual normalization from negative rates |

|

US (Fed funds rate) |

~5.5% |

Peaked mid-2023 |

~3.6% (Dec 2025) |

Tightening cycle ended, cuts in 2024–25 |

|

Europe (ECB deposit rate) |

~4.0% |

Held through 2023 |

~2.0% (late 2025) |

Rate cuts as inflation eased |

The Mechanics of an Unwind

The carry trade is simple in concept but fragile in practice. Its profitability depends on three pillars:

- Wide interest rate differentials – borrowing cheap in yen, investing in higher‑yield currencies.

- Low volatility in the yen – stability ensures predictable funding costs.

- Ample liquidity – easy rollovers and collateral management.

When any of these pillars wobble, the structure can collapse quickly.

- Compression of spreads: As the BOJ hikes while the Fed and ECB pause or ease, the yield advantage shrinks. Suddenly, the diminishing math on the differential starts to undermine the basic strategy as the interest differential becomes highly compressed. A relatively small adverse move can force the participants in the carry play into substantial losses.

- Volatility shock: A sharp yen rally -- triggered by BOJ guidance or JGB yield spikes -- creates mark‑to‑market losses. Stop‑losses scream out for help, margin calls ripple, and leveraged players are forced to unwind positions.

- Liquidity stress: Rising JGB yields and fiscal concerns can tighten domestic funding conditions, making yen borrowing more expensive and less reliable.

The Feedback Loop

The danger is not just the initial move, but the feedback loop it sets off. Imagine a BOJ surprise hike or a fiscal scare that sends JGB yields surging even further. Remember, Japanese investors hold trillions of dollars in foreign assets. If they were forced to repatriate even a modest percentage of these assets, then the yen would rally very sharply against the dollar. Carry books would show losses, forcing a snowball effect of further liquidations. We could see widespread liquidation of positions in emerging‑market FX, high‑beta equities, crypto, global stocks, and pretty much every other major asset class. Prices would fall, volatility would spike, and headlines would frame this development as “The Piercing of the Everything Bubble.” That narrative would accelerate the unwind, even if the fundamentals were not catastrophic.

This loop is self‑reinforcing:

- Yen strength → carry losses → forced selling → global risk‑off → further yen strength as positions are closed.

Likely Magnitudes

Most analysts expect the unwind to be episodic rather than systemic. In a controlled normalization, the yen might rally 5% - 10%, equities could see 5% -10% drawdowns, and crypto might lose 10% - 20% of market cap. Painful, but manageable.

In a sharper FX‑led deleveraging, the yen could rally 15%–20%, equities fall 15% - 20%, and crypto shed 25% - 35%. Emerging‑market currencies would gap lower, especially those with external imbalances.

The tail risk -- a systemic liquidity crunch -- would require a perfect storm: BOJ tightening faster than telegraphed, JGB volatility spiking on fiscal doubts, and global dollar liquidity tightening simultaneously. In that case, the yen could rally 20% - 25%, equities drop at least 20% –30% (my bet is that the drop would be more like 40%), and crypto would lose half its market cap.

Cross‑Market Impact

- Foreign Exchange: USD/JPY is the fulcrum. A disorderly yen rally compresses carry returns and forces unwinds.

- Rates: JGB yields rising toward normalization anchor domestic funding costs. U.S. Treasuries may rally in risk‑off, then reprice as term premia adjust.

- Equities: High‑beta growth and long‑duration tech are most vulnerable. Cash‑rich quality names eventually reassert, but not before drawdowns.

- Crypto: The most sensitive proxy for liquidity. Funding shocks translate into heavy liquidations and sharp market‑cap declines. The total crypto market today is more than $3 trillion. We could expect a minimum drop of 50% in this market, but potentially up to 77%.

- Emerging Markets: FX with external imbalances and high foreign participation are exposed to abrupt funding withdrawal.

- Precious Metals: This would be the surprise market. I could make an argument for gold surging higher – or getting crushed in a massive “sell everything” environment. Therefore, I am withholding my view on these assets for the time being.

- Private Credit: Another victim. This market would get smashed. My best guess – assets would drop by 50% to 77%.

The Narrative Arc

The yen carry trade has lost its easy grace. What once served as a hidden subsidy for global risk-taking now stands as a brittle bridge between Japan’s monetary normalization and the world’s hunger for leverage. Its unwinding may not shatter the system, but it will redraw its contours. The most likely outcome is a series of controlled funding resets -- periodic risk‑off episodes driven by yen strength and JGB volatility. The tail risk is a synchronized shock that forces a massive unwind, but that requires stars to align in a way markets rarely see.

For investors, the lesson is discipline. Funding must be hedged. Collateral buffers must be maintained. Exposure to high‑beta assets must be sized for liquidity shocks. The yen, once the quiet funding currency of choice, has become the tripwire for global liquidity.

Closing Thought

The story of the yen carry trade is the story of complacency meeting regime change. For years, the world borrowed Japan’s silence. Now, as the BOJ speaks with action, that silence is broken. The unwind is not just a market event -- it is a reminder that the foundations of global liquidity can shift, and when they do, they shift suddenly.

Let’s watch carefully how things play out over the coming weeks and months. This unwind, if it comes, will unfold in phases, so we will have plenty of time to get on board. I haven't fully decided that were are going to see this nasty unwind, but I am becomming progressively open to the idea. In the meanwhile, I have built up some modest positions in anticipation of possible risk-off developments in the markets over the coming weeks, but I am primarily testing the waters so far.

As always, I wish you the best of luck with your trading.

Andy Krieger