Takaichi’s Victory – Let’s Put It In Context

Thoughts on the Market

February 9, 2026

Magnitude of Takaichi’s Victory and Its Consequences for the Markets

Every so often, elections provide clarity. What just happened in Japan, however, is truly rare. Sanae Takaichi will be running the country for the next few years with minimal domestic impediments, and with a clear plan of what she wants to achieve. She has a mandate. Whether she succeeds or fails, Japan’s critical role in the global financial system ensures that there will be consequences for everyone.

The fact that this happened at breakneck speed crushes Japan’s reputation for inertia. Four months ago, Takaichi was seen as an outsider in the ruling Liberal Democratic Party’s leadership election. The LDP itself was on the outs, losing its majority in the upper house and relying on shifting alliances to stay in charge.

Today, not only does the LDP have power on its own, but it holds a two-thirds majority in the lower house -- the first time this has ever happened. Takaichi is charismatic and forceful. Comparisons to Margaret Thatcher are apt, but Takaichi one-ups her, because Britain’s Iron Lady never won a mandate this emphatic.

To ram home the magnitude of this shock, Takaichi’s decision to call this election was deemed a gamble. Barely two weeks ago, prediction-market betting put her chance of a simple majority, let alone a two-thirds supermajority, at barely 50%. The shift in her fortunes, and those of the LDP, are monumental.

The critical point after years of drift is that there is no question at all about who is in charge: the LDP runs the country and Takaichi runs the LDP. Takaichi’s majority allows her to overcome not only legislative gridlock, but also bureaucratic inertia. For better or worse, what gets done will be what she wants.

The powerful technocrats know that she’ll be in power for the next few years, so they will give her their full support. This leaves us with the multi-trillion dollar question: where will Takaichi take her country? We know that she is intent on boosting fiscal spending to give Japanese corporations the chance to reclaim some of their global power. Ironically, she is hampered by heavy inflation, which is exactly what the leaders of Japan so desperately sought after thirty-five years of crushing deflation.

Global investors clearly liked her message when Takaichi first got elected PM in October. The Nikkei has surged higher since then, outperforming nearly every market. Based on the nearly 4% rally of the Nikkei last night, however, investors clearly love her commanding victory.

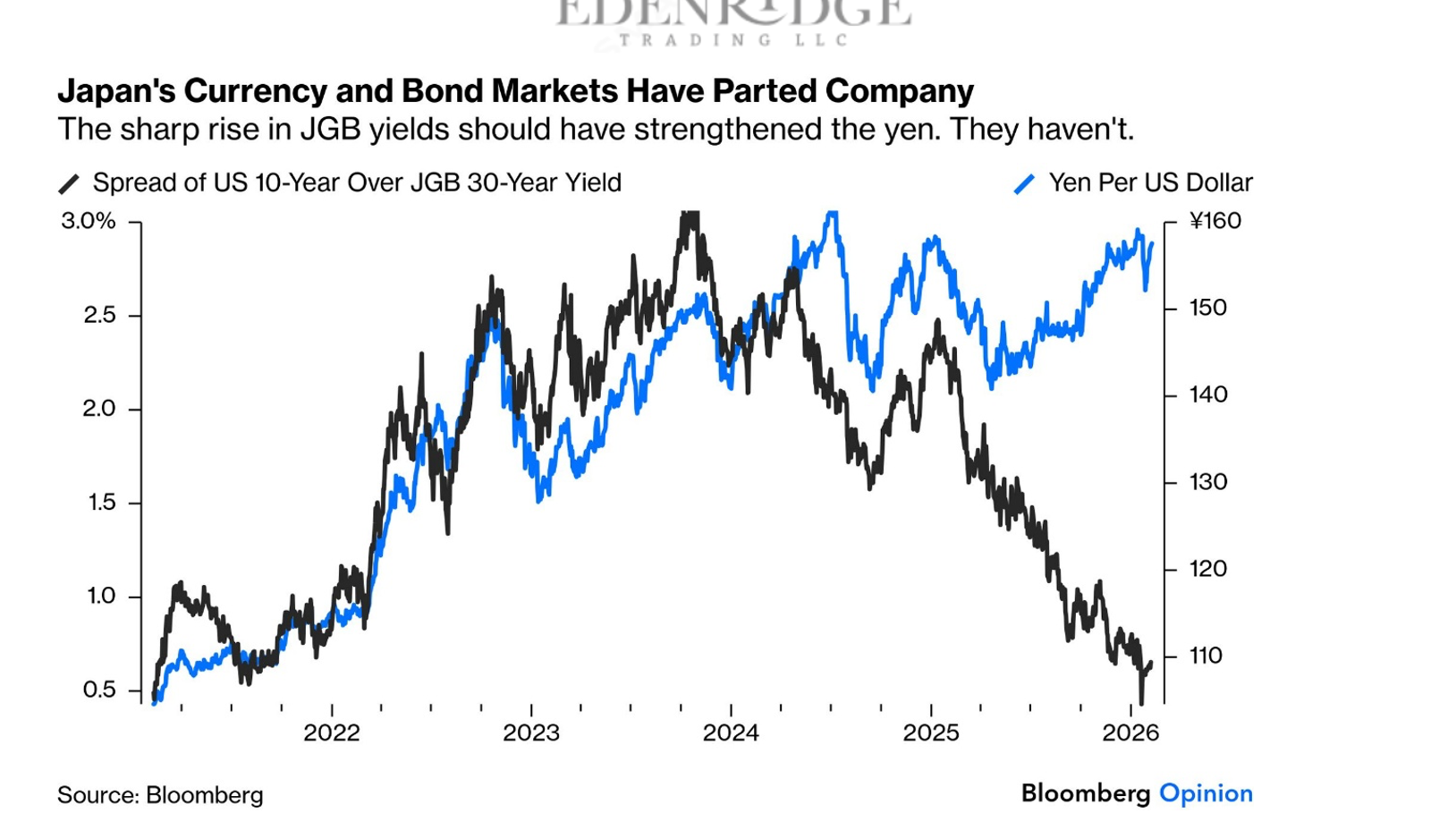

The challenge has been to get the Japanese bonds and the yen to stop hating her message. Her initial election led to a panic sell-off in bonds, with yields screaming higher. You can see from the chart below the absolutely massive spike in yields over the past few months, but you will also see that the bond market seems to have calmed down and adjusted somewhat to the promise of new spending.

The Dollar/Yen chart below shows how the Yen has also been battered badly since Takaichi’s initial election, but interestingly, the Yen has rallied sharply since the news overnight. Many questions persist though, not least of which is how aggressively the Bank of Japan will react to the promised surge in spending. The central bank in Japan is highly cautious, to say the least. In fact, they tend to lumber along slowly like a giant beast, not reacting very much or very quickly to changes in its surroundings.

The relative shift in bond yields would normally have resulted in the strengthening of the Yen, so the Yen's weakness in the past few months suggests that global investors have lost confidence in the way Japan is running its monetary policy. There have been massive amounts of fresh bets in the Yen carry play that were initiated with the expectation that the Japanese bureaucracy would not provide full support to her policies and initiatives. The big question now is whether some of these gigantic exposures will start to get unwound.

The vast power that Takaichi now commands is a game-changer, and could result in a shocking reversal of fortunes for many Japanese assets – not just stocks. We are carrying a very small, long Yen position, and it looks like it might be time to finally build up that exposure – but it isn’t absolutely clear yet how this will play out.

This is one of those times when caution is prudent. Although I am biased towards a large Yen recovery, I can argue that the policy shifts could prove to be very negative for the Yen.

Post‑Election Context: Why This Vote Matters for FX Markets

Japan’s election matters for four reasons:

1. It clarifies the fiscal trajectory

With the powerful mandate, the government can pursue large‑scale fiscal expansion

2. This will shape the BOJ’s operating environment

The BOJ’s normalization path -- already delicate -- will be influenced by:

- political tolerance for higher yields,

- the government’s appetite for debt issuance, and

- the need to maintain financial stability.

3. It influences global capital flows

Japan remains the world’s largest net creditor. Small changes in domestic yields or policy expectations can trigger massive cross‑border flows, moving the yen sharply.

The election therefore acts as a macro catalyst, not a political footnote.

4. If the BOJ moves too cautiously, we can expect further downward pressure on the Yen, with periodic interventions from the authorities being required to keep the Yen’s weakness in check.

If I want to lean towards a Yen bullish scenario, I have to assume that the election becomes a catalyst for fiscal expansion and a new urgency for the BOJ to normalize short-term interest rates aggressively. BOJ normalization, and a re‑pricing of Japan could lead to a credible, higher‑yielding safe haven.

There are multiple major forces which could lead to a gigantic resurgence in Yen strength.

Capital repatriation strengthens the yen

Higher domestic yields will not only reduce the incentive for Japanese investors to export capital, but they will start bringing home some of their trillions of dollars of overseas investments. At the very least, they will start more aggressively hedging the forex exposures of their overseas holdings. At the same time, foreign investors -- long underweight Japan -- continue to increase their allocations to Japanese equities and start to view JGBs as:

- safer,

- more credible, and

- offering positive real returns.

This combination drives enormous net inflows into Japanese assets.

Continued increased global allocations to the Nikkei – without the associated currency hedge would be a powerful Yen positive

The enormous fiscal expansion in Japan, coupled with steadily rising short-term interest rates will lead foreign capital inflows to participate in the Japanese growth story – with one major difference: investors will no longer hedge out the Yen currency exposure due to the narrowing interest rate differentials between Japan and other nations.

Safe‑haven demand reasserts itself

If global conditions deteriorate -- U.S. slowdown, equity volatility, geopolitical shocks -- the Yen will regain its traditional safe‑haven role.

Higher Short-term Yields Accelerate the Unwinding of Yen Carry Plays

This is a critical factor that could lead to a very sharp Yen appreciation.

Market implications

- USD/JPY: multi‑handle decline; sharp downside bursts on BOJ surprises. Short-term rates in Japan head towards 2 ¼%.

- JPY crosses: broad yen strength, especially vs. AUD, GBP, CAD, and high‑yield EM FX.

- Equities: exporters face headwinds; domestic defensives outperform.

5. Investment positioning

- Long JPY vs. USD, AUD, GBP. CAD

- Long JGB volatility.

- Long domestic‑oriented Japan equities; underweight exporters.

- Hedging strategies for corporates exposed to yen appreciation.

Bottom Line – If the government succeeds and stimulates sharp economic growth that is matched by a more proactive BOJ, the Yen will strengthen dramatically. If the government prioritizes fiscal expansion and the BOJ remains cautious, the Yen can remain under pressure.

Both paths are credible. The decisive factor will be how the new government balances growth, inflation, debt sustainability, and financial stability -- and how the BOJ responds.

USD/JPY Forecast Ranges Under Each Scenario

Scenario 1 — A Much Stronger Yen

USD/JPY forecast range (6–12 months):

¥125–140

A move into the 125–140 zone reflects a regime in which:

- The BOJ normalizes more assertively -- allowing yields to rise, reducing bond purchases, and signaling a willingness to tighten if inflation remains sticky.

- Domestic yields rise enough to slow capital outflows and even trigger repatriation from Japanese investors.

- Global risk sentiment softens, restoring the yen’s safe‑haven premium.

- Real yields in Japan turn less negative or even slightly positive, making the yen fundamentally undervalued at current levels.

- Money continues to flow in the Nikkei

In this environment, USD/JPY does not grind lower, it crashes lower, because the market must reprice:

- a more credible BOJ

- a Japan that is no longer exporting capital at scale

- a Japan is even begin repatriating capital.

The lower end of the range (¥125) would require a combination of BOJ tightening and a global risk‑off shock. The upper end (¥140) reflects a more moderate version of the same story.

Scenario 2 – The Continued Weakness of the Yen

USD/JPY forecast range (6–12 months):

¥160–170

Rationale

A move into the 160–170 zone reflects a regime in which:

- The election is interpreted as a mandate for fiscal expansion, with new spending programs and larger supplementary budgets.

- The BOJ continues to move cautiously, prioritizing financial stability and avoiding aggressive tightening that could destabilize JGB markets.

- Japan’s real yields remain deeply negative relative to the U.S. and Europe.

- Global markets remain stable enough for investors to maintain or even increase carry trades, using the yen as the funding currency of choice.

- JGB yields drift higher but not enough to attract foreign inflows – creating a slow erosion of confidence in the Yen without triggering a crisis.

The upper end of the range (¥170) would require:

- sustained global risk‑on conditions,

- a BOJ that remains behind the curve, and

- a government that continues to lean heavily on fiscal stimulus.

The lower end (¥160) reflects a weaker‑yen environment moderated by periodic FX intervention.

My bet is that we end up with the strong Yen scenario winning the fight. I see far too many risks in the system for a sustained risk-on environment to persist without a sharp correction in equities at some point in the relatively near future. I am still not ruling out a rally to 7250/7350 in the S&P500, but the longer we fail to make further headway, the more likely a down move becomes. It is too soon to determine whether this will be a more normal correction like the ones we typically observe during the mid-cycle election years in the U.S., or alternatively, a serious trend reversal.

One thing to bear in mind is that there are currently nearly $100 billion of long equity exposures in the CTA/Hedge Fund community that are close to receiving trend reversal signals due to the markets stalling around current levels. Put simply, they will either be forced to sell if we continue to chop around and go sideways, or if we have a sharp move below 6700 in the S&P500. Their selling would be enough to force further selling as retail players would be squeezed out of their long positions as well. Moreover, if the market’s weakness were to continue, their long positions would not just be forced to flatten, they would also have to flip into short exposures. This doesn’t even address the possible hedging and liquidations of major global portfolios as they continue to diversify away from the U.S. markets. The downside risk is enormous, but it is premature to say that such a move is imminent.

In the meanwhile, I want to wish you all the best of luck as you navigate these very tricky waters.

Best regards,

Andy

********************************

Here you will find Imre’s technical analysis. I strongly recommend that you pay close attention to his work. It is absolutely first rate.

From Imre:

“In my experience, video content is much more valuable than static charts when it comes to building a technical view of the market. Let me know if this format is indeed better for you. All feedback is welcome. This week, I have prepared two videos for you.”

First, we have a recap of last week’s market analysis. This doesn’t happen all the time, but each of the markets that have been analyzed have reached their targets! https://share.descript.com/view/KP1b3DdUgjr

Looking ahead to the next week, I have added the Dollar Index (DXY) and Crude Oil futures into the analytical mix. View this week’s video here: https://share.descript.com/view/KP1b3DdUgjr