THE BUILDING PRESSURE FOR A MARKET BREAKDOWN:Tariffs, Retaliation, De-Dollarization, and the Fracturing of the Global Order

Thoughts on the Market

February 23, 2026

The market is entering a phase where policy instability, geopolitical retaliation, and structural shifts in global finance are converging. The Supreme Court’s ruling against the administration’s tariff authority, followed by vituperative presidential rhetoric, a 150‑day tariff window with 15% tariffs imposed on friend and foe alike, and multiple countries now revisiting bilateral trade deals has created a uniquely combustible environment.

Layered on top of this is the accelerating push by China and its allies to build a non‑dollar trading system, which -- if successful -- will erode U.S. financial power, redirect global capital flows, and set the stage for deeper, more destructive trade conflict.

This report outlines how these forces interact, why they could finally break the market much lower, and what signposts matter most.

1. The Supreme Court Ruling and the Rhetorical Escalation

Many analysts expected the Supreme Court’s decision to invalidate the administration’s tariff authority to have minimal impact on the markets, noting that Trump has many options which he can utilize to reinstall the tariffs that were just declared to be illegal. Instead, the Supreme Court’s ruling triggered a remarkably sharp rhetorical escalation from President Trump, whose public statements have been:

- Vituperative toward trading partners

- Defiant toward the Supreme Court ruling

- Explicitly threatening further action

Markets are not reacting well.

If foreign governments waffle and backpedal on interim trade deals, they should expect escalation -- not moderation -- as the likely response. In fact, a number of major trading counterparties have already called a halt to implementing preliminary trade agreements, with some governments even cancelling planned visits to Washington where they were expected to finalize their negotiations.

A particularly disturbing quote from Trump in his reaction to the Supreme Court’s decision to block his use of sweeping reciprocal tariffs was found in the New Republic, “The court has given me the unquestioned right to ban all sorts of things from coming into our country — to destroy foreign countries.”

This comment was widely viewed as alarming, not only for its tone but for its implications. Trump appeared to suggest that, even without the tariff tool, he retained other powers that could be used to harm foreign economies. The statement came amid broader concerns about his aggressive trade posture, including the imposition of new global tariffs and threats toward NATO allies. This is hardly the sort of rhetoric which builds confidence and trust between trading partners.

The administration is desperately trying to downplay the obvious inflammatory nature of these comments while trying to deflect the other elephant in the room – the utter chaos of reimbursing all the companies for the rollback of the tariffs. We now have the setting for the perfect legal storm as lawyers prepare to go wild as they fight for reimbursements for their clients.

These developments raise the equity risk premium, depress forward multiples, further strain foreign relations, and increase the probability of policy surprise, which is the single most destabilizing factor for risk assets.

2. The 150‑Day Tariff Lifeline: A Built‑In Countdown Clock

The newly announced tariffs come with a 150‑day lifespan. This is not stabilizing -- it is destabilizing.

A tariff that expires in 150 days is:

- Too short for businesses to adjust

- Too uncertain for pricing decisions

- Too political for trading partners to trust

It functions as a rolling threat, not a policy, that raises obvious questions:

· Will tariffs be extended?

- Will they be broadened?

- Will they be replaced with something more aggressive?

Perpetual uncertainty like this is toxic for investment, supply chains, and valuations.

3. Global Backlash: Countries Revisit Bilateral Trade Deals

Multiple countries have now begun revisiting their preliminary bilateral trade arrangements with the U.S. This is the most underpriced risk in markets today.

Retaliation is no longer hypothetical:

- Export‑dependent economies are preparing countermeasures

- Allies are seeking insulation from U.S. unpredictability

- Emerging markets are exploring alternative trade and payment systems

This is how a tariff shock becomes a global macro shock. Trump’s threats to inflict damage on other nations is hardly the recipe for stable relations going forward – even if his threats are just bluster.

4. Tariff Volatility and the “62 Shifts” Claim

Leading financial journals have tallied 62 shifts in tariff policy since Trump took office just over a year ago. A search of credible sources does not confirm that exact number, however the following is confirmed:

- Independent trackers document dozens of tariff changes, reversals, exemptions, and re‑impositions

- The policy regime has been highly unstable

- Businesses and trading partners have faced constant rule changes

For markets, the precise number of shifts and pivots is not the key issue; rather, the pattern is what matters.

There is no doubt that U.S. tariff policy is volatile, unpredictable, and subject to sudden reversal. This erodes confidence and increases the discount rate applied to U.S. assets. The NY Fed just completed its analysis, and they confirmed that U.S. companies and consumers have borne 90% of the tariff cost. In other words, the tariffs are anything but a tax on foreign nations and foreign competitors. Because U.S. investors are bearing nearly all of the pain of the tariffs, their intended purpose -- to level the playing field with international exporters -- has failed dismally. It is not a coincidence that roughly 64% of Americans disagree with the tariff policy.

5. AI Disruption Fears: From Tailwind to Headwind

AI has been the market’s primary multiple‑expansion engine. Now, the narrative is fracturing:

- Concerns about job displacement

- Fears of regulatory intervention

- Recognition that AI creates winners and losers, not simply a universal uplift. Tens of thousands of employees have been laid off, and investors have attacked those companies whose products risk being replaced or commoditized by AI.

- AI mega‑caps dominate index weights, so any de‑rating in the sector can drag the entire market lower.

6. Systematic Selling and Microstructure Fragility

Volatility spikes from tariff shocks and AI fears trigger:

- Vol‑targeting funds to cut exposure

- Risk‑parity models to rebalance

- CTAs to flip from long to short

Additionally, major dealers and market makers are nearly always short gamma as their clients are consistent buyers of puts to hedge a portion of the market’s downside risk. This means that the dealers must sell into declines, amplifying downside momentum.

This is how a 2% down day becomes a 6% -- 8% down week.

7. Earnings Risk and Multiple Compression

Tariffs + retaliation + uncertainty =

- Lower margins

- Lower volumes

- Lower guidance

- Lower earnings visibility

Markets trading at elevated forward P/Es cannot absorb this without multiple compression.

This is the mechanism through which a 10% pullback becomes a 25–35% cyclical bear market.

8. Smoot‑Hawley Parallels: A Dangerous Historical Echo

The Smoot‑Hawley Tariff Act of 1930 raised U.S. tariffs sharply, triggering:

- Retaliatory tariffs from major partners

- A “beggar‑thy‑neighbor” spiral

- A collapse in global trade

- A deepening of the Great Depression

Today’s environment is not identical, but the rhyming elements are unmistakable:

- Protectionist intent

- Retaliation risk

- Policy instability

- Diplomatic deterioration

- Rising global fragmentation

Where Smoot‑Hawley was a single legislative shock, today’s regime is a rolling series of shocks, amplified by:

- A 150‑day tariff fuse

- Legal challenges

- Presidential rhetoric

- Global backlash

Could this morph into a very debilitating situation? Yes -- if retaliation becomes systematic, policy becomes erratic, and global blocs harden.

9. China’s Push for a Non‑Dollar Trading System

China and its partners (BRICS, energy exporters, sanctioned states) are aggressively building non‑dollar trade and payment rails:

- Yuan‑settled commodity trades

- Local‑currency bilateral agreements

- BRICS payment systems

- Expanded yuan clearing networks

This is not theoretical. It is already happening.

9.1. What this means for the U.S.

Erosion of financial leverage The dollar’s dominance gives the U.S. extraordinary power over sanctions, capital flows, and global finance. A credible alternative system dilutes that power.

Reserve diversification If more trade is settled in non‑dollar currencies, central banks need fewer dollars. This reduces structural demand for Treasuries and U.S. equities.

Capital outflows As non‑dollar systems mature, global savings can flow into:

- Yuan assets

- BRICS financial centers

- Regional settlement hubs

Even small shifts raise U.S. funding costs and compress equity valuations. We have already seen this start to play out in the gold market. It hasn’t taken a massive shift out of dollar reserves to drive gold sharply higher to all-time highs.

9.2. How this interacts with tariffs

Tariffs accelerate de‑dollarization because:

- Trading partners seek insulation from U.S. leverage

- Countries fear weaponization of the dollar system

- Retaliation expands from goods to financial architecture

This is how a trade conflict becomes a systematic conflict.

9.3. Which of these factors pose near-term risks?

- Escalating tariffs and retaliation

- Accelerating non‑dollar trade systems

- A U.S. response that doubles down on coercive tools

This would fracture the global order into competing blocs, raising:

- Volatility

- Funding costs

- Risk premia

- The probability of severe trade and financial crises

10. The Downside Path: How the Market Could Break

Stage1: Sentiment fracture (now)

Tariffs + rhetoric + AI fears → volatility spike → 5–10% decline.

Stage 2: Mechanical de‑risking

Systematic selling accelerates → liquidity pockets → 10–18% decline.

Stage 3: Earnings reset

Guidance cuts + margin pressure → 18–25% decline.

Stage 4: Global retaliation + de‑dollarization loop

Trade blocs harden → capital flows shift → 25% -- 35% decline.

This is the full‑cycle bear market scenario—not guaranteed, but now materially more plausible. Could the ultimate decline be greater than 25% to 35%? Yes. In fact, I wouldn’t be shocked if at some point we see the market correct all the way back to levels last seen during the Great Recession. That would take a long time, and it would be very painful for nearly everyone, but it cannot be ruled out as a possibility.

11. Key Signposts to Watch

- Foreign retaliation announcements

- Treasury market stress or widening credit spreads

- Persistent volatility above recent norms

- Deleveraging of AI mega‑caps

- Broadening of array of companies that can be damaged by AI developments

- Accelerating yuan‑settled trade

- Negative corporate pre‑announcements

- Diplomatic breakdowns or tariff extensions beyond 150 days

When three or more of these signposts align, the probability of a severe market break rises sharply. I previously wrote about the five stages that I see as preconditions for a sharp market sell-off, but these signposts should not be ignored. Doing so could be a grave error as any of them could turn out to be the final trigger.

The points I am covering here don’t even begin to address the massive bubble that has been artificially generated by the authorities with the implementation of their wild monetary and fiscal policies in their effort to permanently forestall recessions and economic downturns. Borrowing and recycling tens of trillions of dollars into the economy through massive debt financing while pumping trillions of additional dollars into the banks through aggressive monetary stimulus is a policy mix that is bound to end in tears.

This hyper-aggressive blend of fiscal and monetary policy was bound to create massive bubbles. As a result, we have dramatically distorted valuations in real estate, equities, commodities, and crypto assets. We have already seen the Bitcoin bubble burst, but the other markets are still hanging on – albeit tenuously. Their valuations are extreme, and these dangerous policies have created a bifurcated economy that is divided into the wealthy and everyone else. This toxic condition brings its own host of problems. In any event, it is just a matter of time before the other market bubbles burst as well; at which point we will have a real crisis on our hands. If I were to identify any one particularly vulnerable sector right now, I would probably choose the private credit market. It has grown enormously, now comprising more than $7 trillion in total assets – and it is showing some serious signs of weakness and vulnerability.

Conclusion

The market is no longer dealing with isolated shocks. It is dealing with a convergence of destabilizing forces:

- Tariff volatility

- Presidential escalation

- Legal uncertainty

- Global retaliation

- AI narrative fracture

- Systematic selling

- De‑dollarization

- Historical parallels to Smoot‑Hawley

- Dramatic bubble conditions in multiple asset classes

Any one of these could cause turbulence. Together, they create the most fragile macro environment in years.

I want to wish you all the best of luck as you navigate these treacherous market conditions. In the meanwhile, please carefully read through Imre’s analysis. His insights are very, very helpful as another way to make sense of some very tricky markets.

Andy Krieger

************************

Imre’s Analysis

Thank you to everyone who has written in with thoughtful questions about my approach to the markets.

This week I’m going to answer them directly, by laying out what I focus on as both a market analyst and a trader:

First and foremost, I trade participation, not price.

Most traders trade price bars.

They buy breakouts because a line was crossed.

They fade moves because a wick printed.

They chase momentum because a candle expanded.

They anchor to narratives because a headline hit.

It sounds logical. But their results are all over the place. It feels random because they are engaging with the market at its most superficial layer.

Let’s think this through.

If most traders fail over time, the default assumption should be simple. Doing what most traders do produces the most common outcome. And yet the vast majority are running the same playbook.

Same inputs.

Same interpretations.

Same mistakes.

Here’s the difference in my process…

I do not start with price; I start with structure.

To understand what I mean by that, you have to see markets for what they are. They are auctions. Nothing more. Nothing mystical. An auction is simply a process of discovering price through participation.

Buyers and sellers transact. When they agree, trade builds. When they disagree, price moves. That is the entire mechanism.

When heavy two-way trade builds at a level, that level becomes accepted value by both buyers and sellers. When participation dries up, price moves in search of the next area of agreement. Most traders are reacting to the movement itself.

I am asking a different question.

Is the auction building value here, or failing to do so?

Markets constantly rotate between two conditions: balance and discovery.

Balance is agreement.

Discovery is imbalance.

Inside balance, two-sided trade dominates. Price rotates. Movement is contained.

There is no structural edge in the middle of balance.

There is only noise.

Edge exists at the boundary — where agreement is tested.

When price reaches the edge of a balanced range, only two outcomes are possible.

Participation expands and value begins building at new prices.

Or participation dries up and price rotates back into prior agreement.

That is the entire decision tree.

How far price moves alone does not tell you which one is happening.

A fast move is not proof.

A spike is not proof.

A breakout is not proof.

Acceptance requires time.

Acceptance requires participation.

Acceptance requires structure to hold.

If value builds beyond a structural boundary, the auction is migrating.

If it cannot build, the auction rotates.

That is what I am measuring.

Not breakouts or reversals.

Not headlines.

Not emotion.

Participation.

To keep things simple, let’s apply this framework to one market for the week ahead.

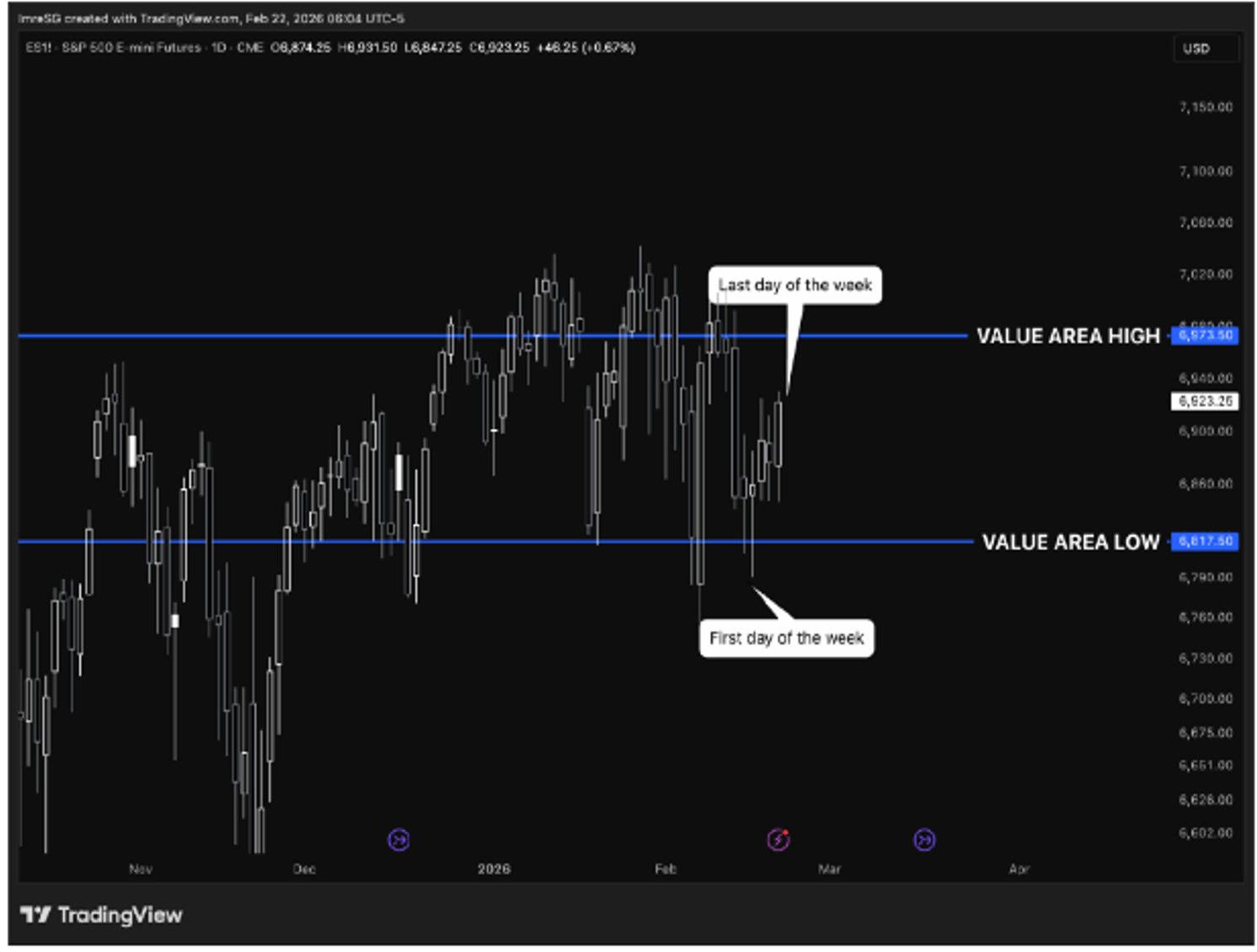

The S&P 500 e-mini futures (ES).

Last week, the key observation was that the market remains in a balanced regime.

In a balanced state, rejections of the extremes of fair value tend to produce rotations from one

extreme to the other. This is known as a value traverse.

Last week’s upper boundary of value was 6973.50.

The lower boundary was 6817.50.

As the week opened, price tested 6817.50 and rejected it.

That rejection set up the traverse — a rotation from the lower boundary back toward 6973.50.

The week ultimately closed at 6923.

That is what balance looks like:

This past week provided ample opportunity to de-risk and lock in profits.

While I do not trade headlines, I respect how quickly markets can move through thin liquidity following unexpected news.

Rising geopolitical tensions, including the potential for U.S. conflict with Iran, may increase volatility.

But volatility does not equal imbalance.

The broader regime remains balance.

And until that changes, the levels remain the same.

My best trades will come from the edges of value — 6817.50 and 6973.50.

I am not interested in trading the middle of this range.

Balanced markets do not last forever.

Eventually, one side exhausts and the auction shifts into imbalance.

That is when sustained migration begins.

Until then, patience.

There will be opportunity.

Do not rush the trade.

Let the market commit first.