The Dangerous Issues the Fed Is Not Addressing

What is really happening here? Why might the Fed want to embark on such a dangerous path?

I am warning you in advance that you might not want to read today’s newsletter. There are many things in it which are highly disturbing. Although all of the data in it is supported by publicly available information, I suspect that if you read through the whole write-up, you will be left with a strong feeling of concern and anxiety because there are things taking place right before our eyes that should make every one of us deeply concerned about our collective future.

Federal Reserve Chairman Jerome Powell held a news conference this past Wednesday, the 20th of March, after announcing that the Fed would hold rates steady for the fifth consecutive meeting. He also made it clear that he would persist with the Fed’s commitment to lower rates multiple times later this year. These decisions were highly anticipated, so the event didn’t sound particularly newsworthy. Still, as I watched it, I sat transfixed, unable to shift my focus, as I really couldn’t believe what I was hearing, or rather what I wasn’t hearing.

I understand why the various members of the media failed to press the Fed Chairman more vigorously with their questions. They are professionals trying to report on a very important news event, so they naturally don’t want to lose their access to the Fed by posing overly aggressive or overtly controversial questions. I also understand why Powell would want to handle the questions in his typically cool, calm, and collected fashion. In fact, Powell is truly masterful at deftly avoiding any topics that might force him to discuss things that he doesn’t want to address in a public setting. As a result, the press conference was more like a genteel chat that didn’t dig very deeply into very important matters that affect us all, and it certainly didn’t even begin to address a number of critical issues that were left unsaid.

Powell, as the Chairman of the Federal Reserve Board, has a dual mandate – maintain price stability and maximum employment. Price stability means that inflation remains low and stable over the longer run. When inflation is low and stable, people can hold money without having to worry that high inflation will erode its purchasing power. In simple terms, inflation is a rise in prices, which can be translated into the decline of purchasing power over time. The rate at which purchasing power drops can be reflected in the average price increase of a basket of selected goods and services over some time.

I have written at length about the farcical idea that a 2% annual inflation rate is equivalent to price stability. It is an arbitrary, contrived notion that resulted from an off-the-cuff comment from a central bank governor, who frankly, never should have been the head of the central bank in the first place. In the second place, he got lucky that structural, widespread disinflationary pressures were in force that would naturally lower the rate of inflation from double digit levels to low single digit levels. His “forecast” of 2% inflation proved to be right through pure coincidence.

In general, 2% inflation is a rate of price increases that is tolerable to most consumers in the short term, but over time, it is crushing. With 2% annual inflation, the buying power of our money is halved over thirty-five years. Any inflation, even at a 2% annual rate, hurts the poor people the most since they are least likely to own assets that will appreciate over time to offset the loss of their buying power. It is a classic example of the boiled frog syndrome as the slow and steady cooking doesn’t force the frog to immediately jump out of the water, but after a while, the frog dies from the heat.

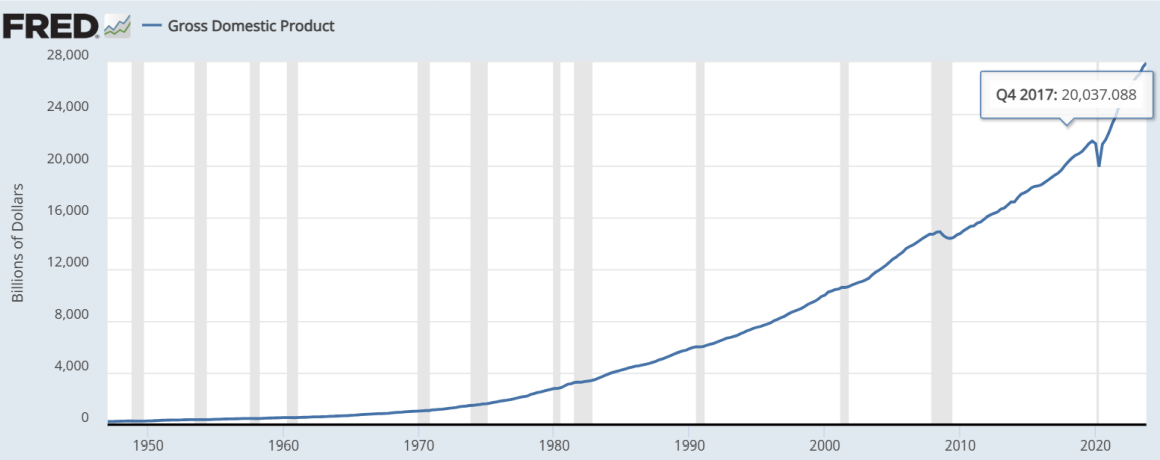

There are substantial benefits that flow from this policy of moderate inflation over time, but unfortunately these benefits only flow to the political leaders and the rich. Political leaders can point to the fact that the economy seems to be doing better even when it is not. They can note that wages for workers are rising and that the GDP is increasing. They just forget to point out that the costs of homes and many goods and services are rising faster than the wages. They also forget to point out that the GDP is rising because the government keeps borrowing and spending more and more, supported by the central bank’s easy monetary policy, thereby fueling a growing, long-term problem for the citizens. As we will see later in this write-up, the cumulative impact of this so-called price stability is that homes are now the least affordable they have ever been. The rich people who hold assets that are appreciating in value, however, love this scenario, and they are happy to support the people who are in power.

The Fed has been trying to deal with a very serious inflationary problem for the past three years, as the pace of the price rises has been way beyond what most people can tolerate, and there has accordingly been a lot of howling from consumers who are feeling the pain. Powell is very sensitive to his reputation, and he bristles at the idea that he one day he might be compared to former Fed Chairman Arthur Burns rather than the highly revered Paul Volcker. Even when inflation was surging in 2021, Powell, as well as other Fed and Treasury officials, characterized these price increases as “transitory.” Powell even went so far as to refuse to admit there was any inflation in the economy. For example, at a press conference on July 28, 2021, Powell tried to explain away his frequent usage of the term “transitory” when he talked about the nation’s inflation. He desperately tried to portray the dramatic price rises in our economy at that time simply as “price increases,” but not as “inflation.” Huh? Seriously? In a classic example of doublespeak, he noted, "The concept of 'transitory' is that price increases will happen. We're not saying they will reverse, but the process of inflation will stop.” Of course they won’t reverse. He wants prices to keep rising, just not quite as fast. He then summed up his argument by saying, “What has happened in the past year is an example of ‘a price increase but not inflation…” Powell may be a lawyer and not an economist, but he surely knew his argument was idiotic.

Did he seriously think that was a sensible way for the Fed to deflect any blame or responsibility for the severe inflation that hundreds of millions of Americans were experiencing – and from which they are still suffering today. This suffering is real and palpable, and more than half of our country experiences this pain every time they go to the supermarket or try to pay their ever-growing bills. The rate of price increases since that time may have moderated, but it is still way too high, and it doesn’t lessen the pain that these price increases continue to cause.

I was horrified by the explanation then, and I am still horrified that arguably the most powerful person in the western world could be so dismissive of the painful impact of the Fed’s policies. What did the Fed think was going to happen when they pumped $4.8 trillion dollars into the system at the same time the Treasury Department was borrowing and spending money at an unprecedented pace? Sure, there were supply bottlenecks due to Covid, and some of these price increases were a direct by-product of these bottlenecks. Uncontrolled government spending and essentially limitless liquidity, however, were bound to lead to widespread inflationary pressures at some point. It was only on November 29, 2021, during a Senate testimony, that Powell finally came clean and offered to “retire” the usage of the word “transitory” to describe the inflation in the US. During that testimony, Powell finally confessed that the inflation had spread to multiple sectors of the economy, and that it needed to be addressed. “The economy is very strong and inflationary pressures are high,” Powell said, noting that the pandemic-induced supply chain bottlenecks that caused a surge in prices for goods like used cars, but that the rising price pressures had become widespread. This preceded the aggressive rate hikes that followed in 2022 and 2023.

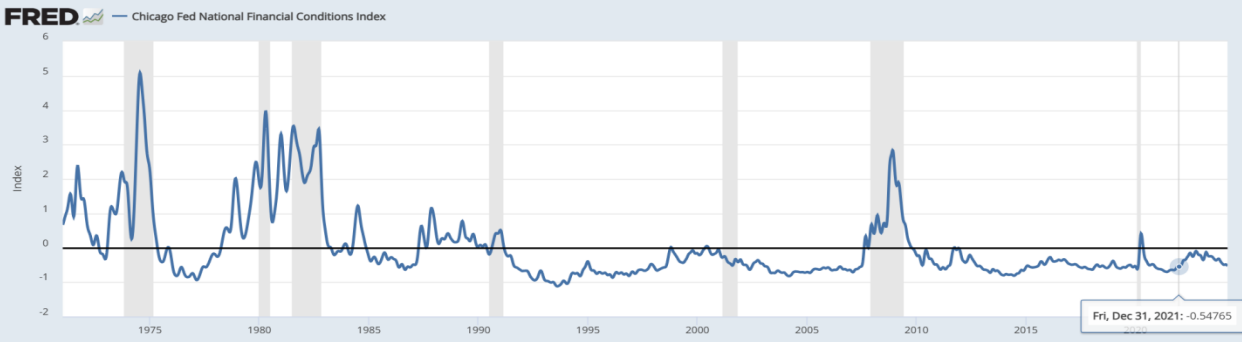

For sure, the inflationary pressures of 2021 and 2022 have eased somewhat, but they are still exceedingly high, and the cumulative price increases are a serious problem for much of our country. Inflation is still way above the Fed’s target inflation rate of 2%, and recent inflation data showed signs of picking up. Our unemployment level is below full capacity. Housing is less affordable than it has ever been. Most importantly, though, the Fed’s own financial condition index shows us that we now have some of the loosest financial conditions ever. In fact, as you can see in the chart below, financial conditions are now as loose as they were before the Fed started hiking rates in 2021.

The variables in the Fed’s Financial Conditions Index (FCI) include the federal funds rate, 10-year Treasury yield, 30-year fixed mortgage rate, triple-B corporate bond yield, Dow Jones total stock market index, Zillow house price index, and nominal broad dollar index. The weights capture the estimated effects of unanticipated changes in each variable on real GDP growth over the subsequent year. It is designed to measure the overall level of financial stress in the economy. Given the current market conditions, per the Fed’s own index, there is absolutely no reason for the Fed to even consider cutting rates at the current time, let alone curtailing its balance sheet reduction plan. In fact, the FCI has been trending downward since the start of 2023, indicating a loosening of financial conditions despite the Federal Reserve's aggressive rate hikes.

As noted, the Fed’s own measure, financial conditions are the loosest they’ve been since the end of 2021. Stock markets are making new all-time highs on a regular basis. (At last count, the S&P has made 20 new all-time highs this year alone.) Inflation has been picking up. Growth projections for 2024 have been raised. Large investments are planned in new sectors such as artificial intelligence, ship building, green energy initiatives, and many other areas, and there are abundant sources of capital available.

Clearly, Powell is very familiar with these facts. It is his own organization’s index, so he knows full well that there is absolutely no sensible explanation for the Fed to cut interest rates at the current time. Monetary conditions are among the loosest they have been in many decades, yet Powell told us that the Fed is still targeting three interest rate cuts this year, another four cuts next year, and furthermore, the Fed intends to curtail its so-called Quantitative Tightening by terminating its balance sheet reduction in the near future.

If anything, the Fed should be hiking rates, not lowering them. Their balance sheet is still way too large, and the wealth effect of the stock market’s surging prices is enormous, so what is really happening here? Financial conditions are extremely loose. Treasury is still spending at an insane pace. Why might the Fed want to embark on such a dangerous path?

Remember, Powell encouraged the recent surge in stock markets in the 4th quarter of last year when he talked about the likelihood that the Fed would lower rates this year multiple times while knowing very well how loose financial conditions were at the time. He talked about the downward path of inflation, and he used that as an excuse to embark on this foolhardy plan. He has had many opportunities since then to dampen the animal spirits, but instead he keeps feeding them. Momentum-based buying has spread across many markets, and prices are surging to new all-time highs in crypto and a number of commodities. If things end badly with a nasty meltdown, then enormous blame is going to get piled onto Powell and the Fed. Things may seem great now, but are they? Is it really so hard to imagine a scenario in which we quickly descend into an ugly condition of stagflation? What could really be behind Powell’s process?

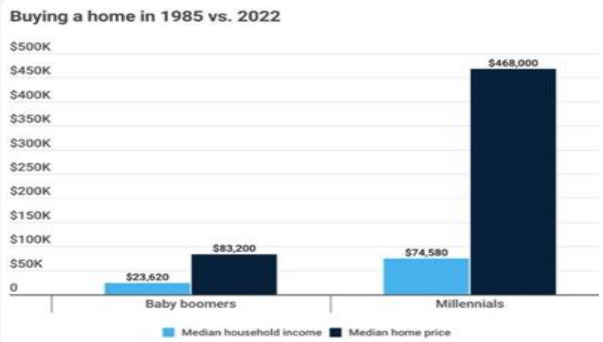

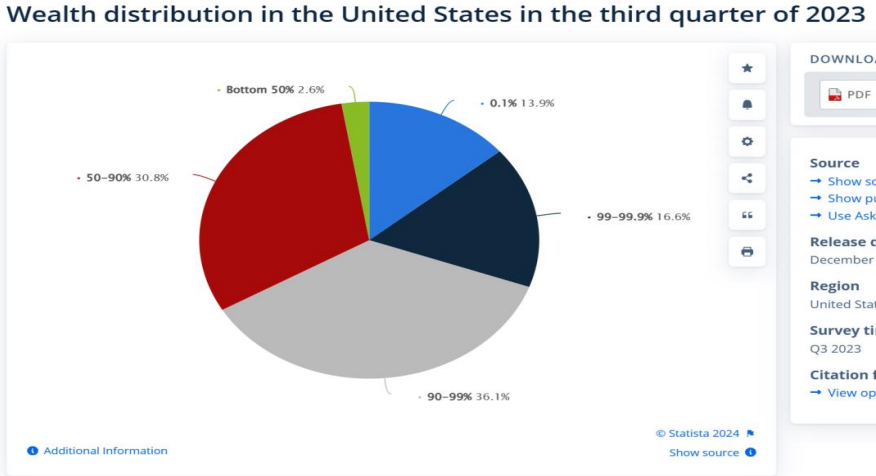

The wealth disparity in the US is staggering, and frighteningly similar to the period right before the Great Depression. I referred earlier to the unaffordability of the current housing market. Have a look at this simple chart.

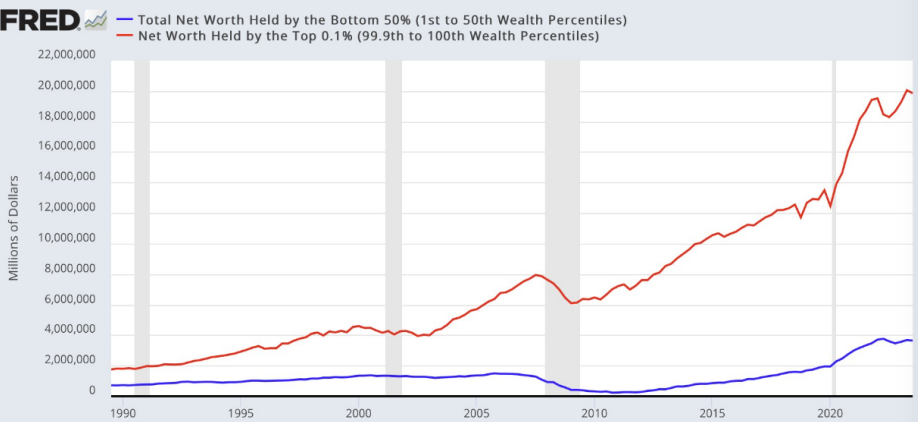

Aside from the challenges of being able to afford a house, consider the distorted levels of wealth held by the top .1% of the country’s population. Their wealth dwarfs the collective wealth of the bottom half of the country. Is this disparity really something that is sustainable? Is it healthy? Do I want my children and grandchildren to live in such a class society? My answer to all three is a resounding “no.”

The wealth disparity is astonishing. This data comes from the Fed, so they are well aware of this situation. According to Stanley Druckenmiller, the Federal Reserve Bank of the United States has played the leading role in exacerbating economic inequality. Druckenmiller, a billionaire hedge fund manager, asserts that the Fed’s policies have disproportionately benefited the wealthy while leaving the less affluent behind. Druckenmiller stated during a keynote speech at the USC Marshall Center for Investment Studies’ Student Investment Fund Annual Meeting:

“I don’t think there has been any greater engine of inequality than the Federal Reserve Bank of the United States in the last 11 years. Everyone wealthy that I know is making fortunes because this guy [Fed Chair Jerome Powell] is printing money like there’s no tomorrow. The kids in Harlem are not benefiting from money-printing, but wealthy people are.”

He points out that the ultra-wealthy have been amassing fortunes due to the Fed’s aggressive money-printing practices, while everyday citizens, especially those in economically depressed communities, have not reaped similar benefits.

Druckenmiller has consistently criticized the Fed for its role in perpetuating inequality. Back in 2013, he accused the central bank of “robbing the poor to pay the rich.” His concerns center around policies like quantitative easing, which inflate asset prices and primarily benefit wealthy investors.

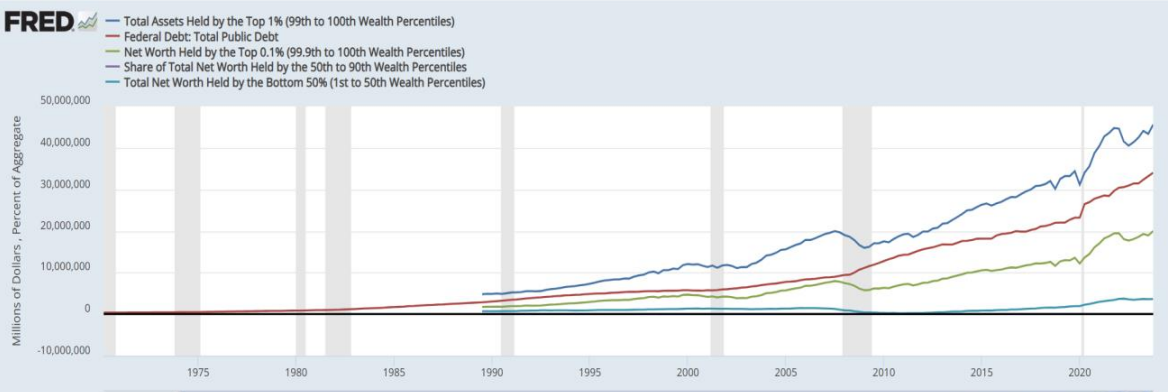

The next chart illustrates the situation in even more detail. The total assets of the top .1% of the citizens absolutely dwarf the assets of the bottom 50%. The total assets of the top 1% present an even more overwhelming disparity.

In fact, one might go so far as to say that the Fed has sold out the citizens of the United States for the benefit of the nation’s wealthy elite. Perhaps there is a separate political agenda at play here as well, although the stock market’s stellar performance will not guarantee a victory for the incumbent candidate due to its overwhelming ownership being controlled by a very small percentage of the nation.

The average consumer is paying dearly for these policies, and the long-term prospects for the US are frightening. Extreme wealth inequality has led to civil unrest many times in many nations, and the US could very well face an existential challenge if the current imbalances continue to grow unchecked. In the 1930s, during the Great Depression, over half of the wealth disparity got wiped out, and we should not consider ourselves immune from such an occurrence.

Aside from adhering to policies that clearly favor the rich, even some of the data that the Fed relies on for a portion of its inflation data distorts reality. In 1983, mortgage costs were removed from the CPI. Larry Summers, the former Secretary of Treasury and former President of Harvard University, conducted a study to reconstruct the CPI and adjust for housing borrowing costs. Per the Bureau of Labor Statistics, the adjusted inflation data from 2023 was roughly 18%, and the current inflation rate would be around 8% on an annualized basis. In other words, if we used some of the prior inputs, we would recognize that inflation is far worse than we think.

In terms of other puzzling things, the Fed has an army of economists on staff, and they have access to all of the best technical analysts in the world. Yet, Powell chose to give the equity markets yet another push this week even though the S&Ps are trading at all-time highs with essentially unsustainable, overbought market conditions. Weekly readings on the S&Ps, with RSIs at 80% are already in nosebleed territory. Impelling more buying at these levels is a great way to ensure that bubble-like market conditions will ensue. It is almost as if someone threatened him to drive the markets higher – or else.

In fact, what Powell told us on Wednesday was that he really doesn’t care that inflation readings have recently come in hot. Moreover, we might as well forget about the 2% inflation target because he is going to tolerate a much higher level of inflation no matter what. Essentially, he has shifted his stance to one in which he now intends to reach his 2% inflation target at some undefined time in the future, but he is in no hurry. In case we had any doubts, he has a very clear agenda for the time being, and it is not geared towards helping the bottom 50% of the nation.

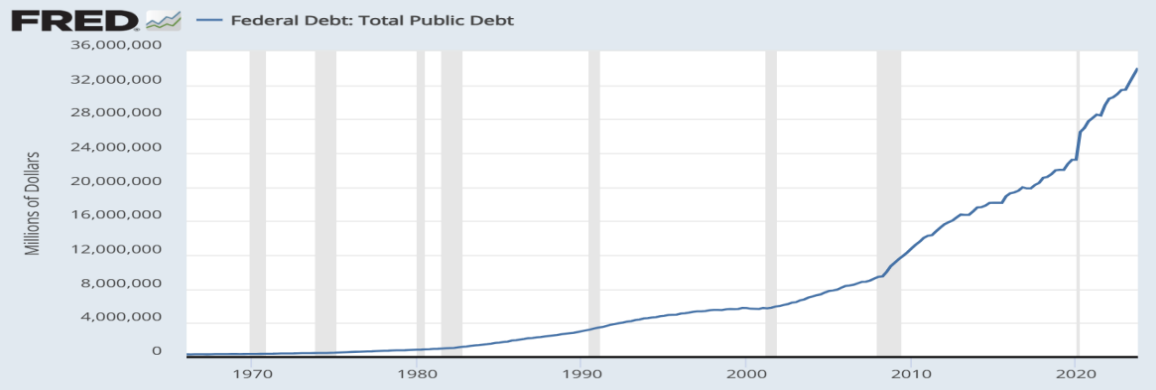

The dates don’t align perfectly in the two charts above, but the overall picture is very clear. The huge increase in Federal Debt aligns almost perfectly with the growth in GDP, which further aligns with the massive rise in wealth inequality. The extent to which the top 1% has benefited so much from the growth in GDP leads us to the obvious conclusion that the massive Federal Debt has overwhelmingly favored the wealthiest people.

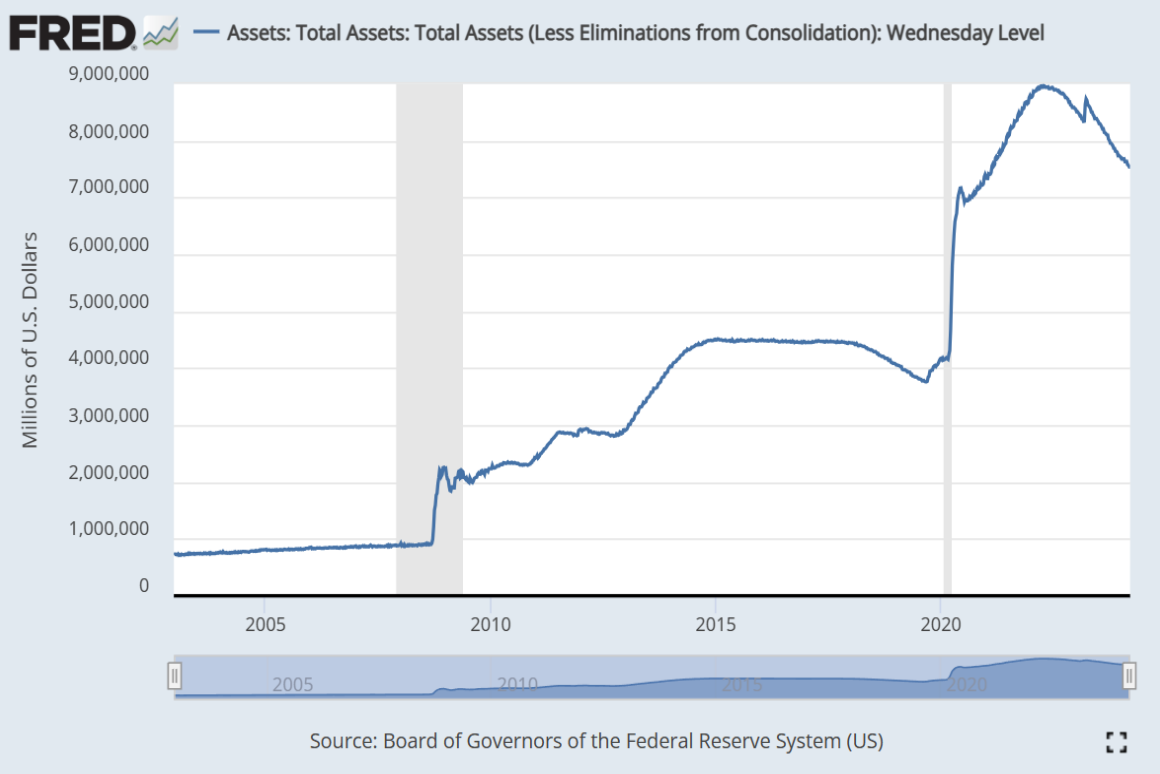

The next chart further adds further support to the contention that the Fed is an engine of wealth disparity in our nation. In fact, when one looks at the growth of the nation’s federal debt, the growth of the Fed’s balance sheet (below), and the growth of wealth of the top 1%, one can easily conclude that the system is heavily weighted in favor of the wealthy, if not rigged in their favor.

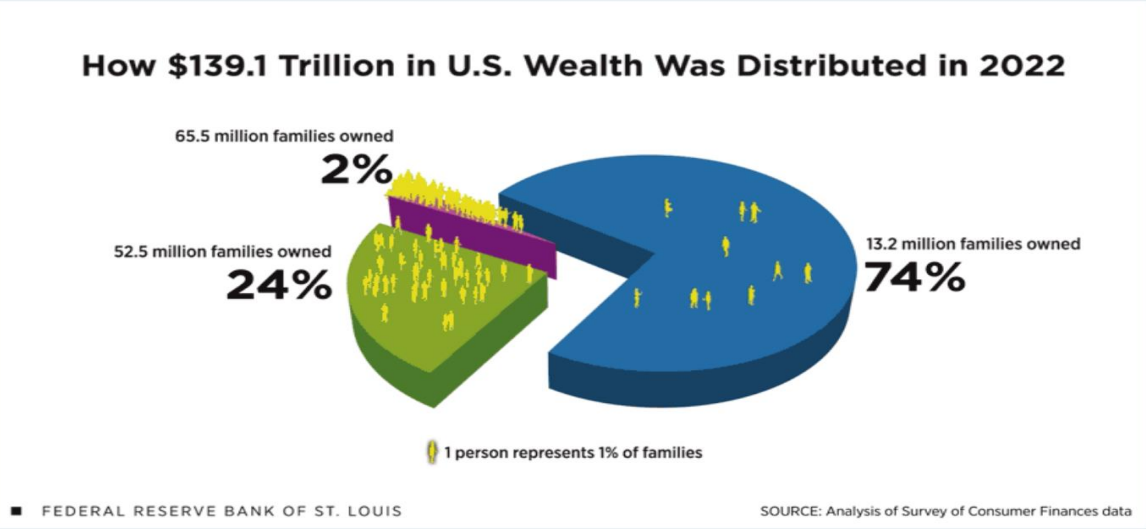

These are disturbing observations, but they seem incontrovertible. In case the prior charts weren’t clear, the chart below from the Federal Reserve Bank of St. Louis is very, very clear and easy to understand. Our nation’s wealth disparity is shocking.

Business Insider summarized this situation quite nicely with the following information. In this case, it pertains more specifically to stock market holdings.

Given that the top 10% of American hold 93% of all stocks, it is really clear who the authorities are speaking to when they brag about how well the stock market is performing. This fact is clearly of little or no consequence to the bottom 50% of Americans. So who is really representing their voice?

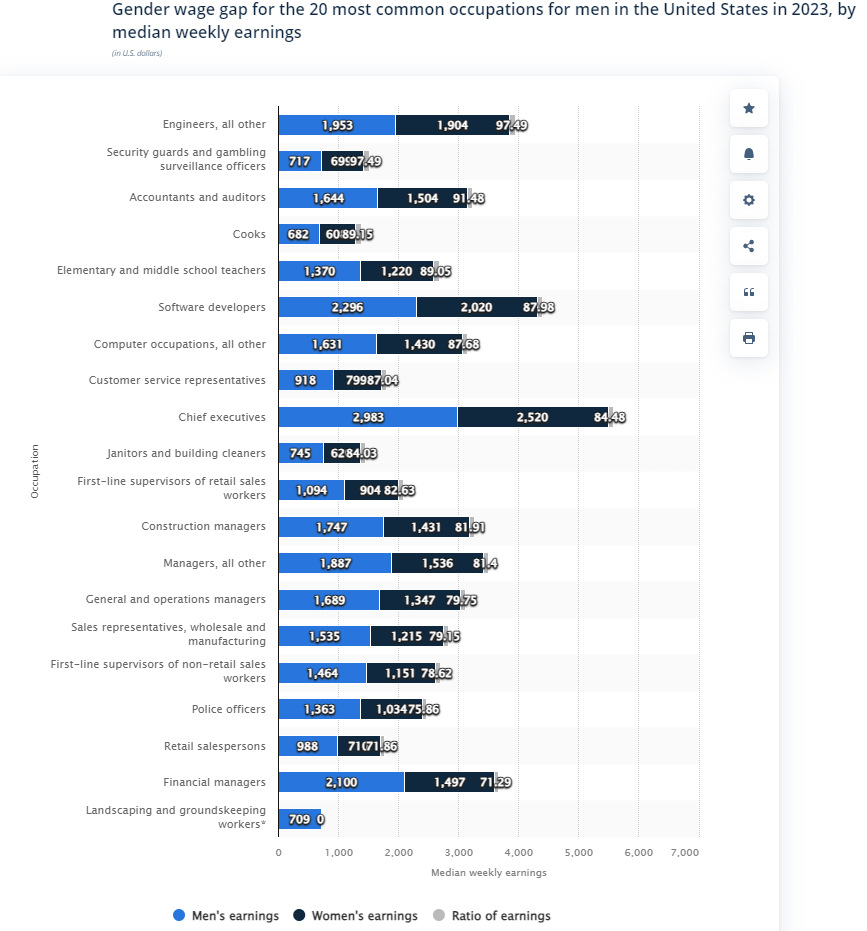

Just in case I haven’t pushed enough buttons yet, consider the following gender wage gap. With five daughters, I must say that I find this gap particularly galling.

I will leave you with one more illustration about the lack of affordability of homes in today’s market from Business Insider.

In my view, America's growing wealth inequality is a consequence of central bank market intervention/manipulation and distorted fiscal policies that favor the rich, and it is increasingly dangerous from a social and societal perspective. The gender pay inequality is a slice of the inequality, but not the essential component. Yes, it needs to be addressed, but the dramatic disparity between the mega-rich and the rest of the population is unsustainable. Based on historical precedent, this is likely to end in one of several ways; either we have a catastrophic crash in multiple markets that resets the balance somewhat, or we have serious social unrest that leads to a forced rejiggering of assets across the population.

There is one alternative reason that might be driving the highly peculiar and dangerous Fed and Treasury policies right now, and that reason might be related to a monstrous banking or federal funding problem that is lurking just below the surface. The authorities could be trying to cover it up for fear of creating a panic. Perhaps it is a combination of massive losses due to CRE commercial loan obligations which are facing unprecedented stress, bank liquidity problems due to balance sheet problems from the huge unrealized and hidden losses in the banks’ “Held to Maturity” portfolio, or an anticipated problem with the Treasury refinancing its gigantic debt maturities in 2024/2025, or any of a host of other possible issues. None of these scenarios sound particularly appealing as social unrest due to wealth disparity or banking meltdowns is hardly a desirable choice, and all the alternatives would negatively impact large swaths of the population.

Perhaps the authorities decided that higher inflation for a while longer is far better than the alternative. Either way, it is time to pay close attention to what isn’t being said and take a more cautious approach with our speculative investments.

I will revert to my more typical write-up next week.

Wishing you all the very best.

Andy Krieger